AI-driven marine war risk pricing helps insurers and shippers respond to Black Sea drone threats, route detours, and AIS spoofing with real-time risk scoring.

AI for Marine War Risk: Pricing Drone-Era Routes

A 350-mile detour doesn’t sound dramatic until you realize it’s a 70% longer run across one of the world’s most contested bodies of water.

That’s what’s showing up in recent vessel tracking: oil tankers hauling Russian crude across the Black Sea are hugging the coastlines of Georgia and Turkey instead of running the more direct route to the Bosphorus. The reason is brutally practical—reduce exposure to Ukrainian sea-drone attacks—and it’s a perfect snapshot of what supply chain risk looks like in late 2025: not theoretical, not annual-review stuff, but a live operational decision made route-by-route.

For insurers, brokers, and risk teams, this is where AI in insurance stops being a buzzword and becomes an operating system. When routes shift overnight, when AIS signals can be spoofed, and when war risk pricing can jump on a headline, you need tools that can ingest real-time signals, quantify exposure, and respond faster than the threat cycle.

Why tanker detours matter to insurance pricing (and procurement)

The key point: route changes don’t only move ships—they move risk, cost, and contract terms.

A tanker running close to shore may reduce exposure to certain threats (for example, specific drone operating patterns), but it can increase other exposures: coastal congestion, navigational hazards, surveillance intensity, and choke-point sensitivity near the Turkish Straits.

From an insurance and procurement standpoint, a detour triggers a cascade:

- More time at sea → higher exposure window for hull, machinery, and war risk per voyage

- Higher fuel and operating costs → freight rates rise, which hits landed cost models

- Schedule volatility → knock-on effects for refinery intake planning and storage

- Changed aggregation risk → more vessels clustered along the same corridor

This matters because supply chain and procurement teams often treat insurance as a fixed line item. In reality, marine insurance and war risk insurance behave like a floating price, tied to movement patterns, threat intelligence, and sometimes sudden market tightening.

War risk is now a routing variable

War risk used to be something you reviewed with your broker periodically. Now it’s something operations teams indirectly manage through routing decisions.

In the Black Sea, recent reporting shows multiple Russia-linked vessels have been attacked by sea drones—often when empty, which is a reminder that attackers may be targeting capability, signaling, or disruption potential rather than just cargo value.

Insurers respond to this with:

- tighter underwriting rules on voyages and ports

- higher additional premiums for listed areas

- more scrutiny of vessel identity, ownership, and management

- faster changes to terms based on incident frequency

The reality? If your underwriting and pricing process can’t adjust at the speed of route change, it’s already behind.

The data problem: AIS spoofing, “unknowns,” and fast-changing exposure

The key point: marine risk modeling fails when you can’t trust location and identity data.

Vessel tracking commonly relies on AIS broadcasts. But in the current conflict environment, false digital positions are increasingly common. In the specific case highlighted by recent satellite imagery, a vessel’s physical location appeared to diverge from its reported position by several nautical miles within minutes.

For insurance and risk teams, that creates three hard problems:

- Exposure uncertainty: If you can’t confirm a ship’s path, you can’t confirm whether it entered a high-risk zone.

- Claims friction: Disputed voyage paths complicate claims investigation and coverage triggers.

- Counterparty risk: If beneficial ownership and insurer are unclear, recovery and compliance become messy fast.

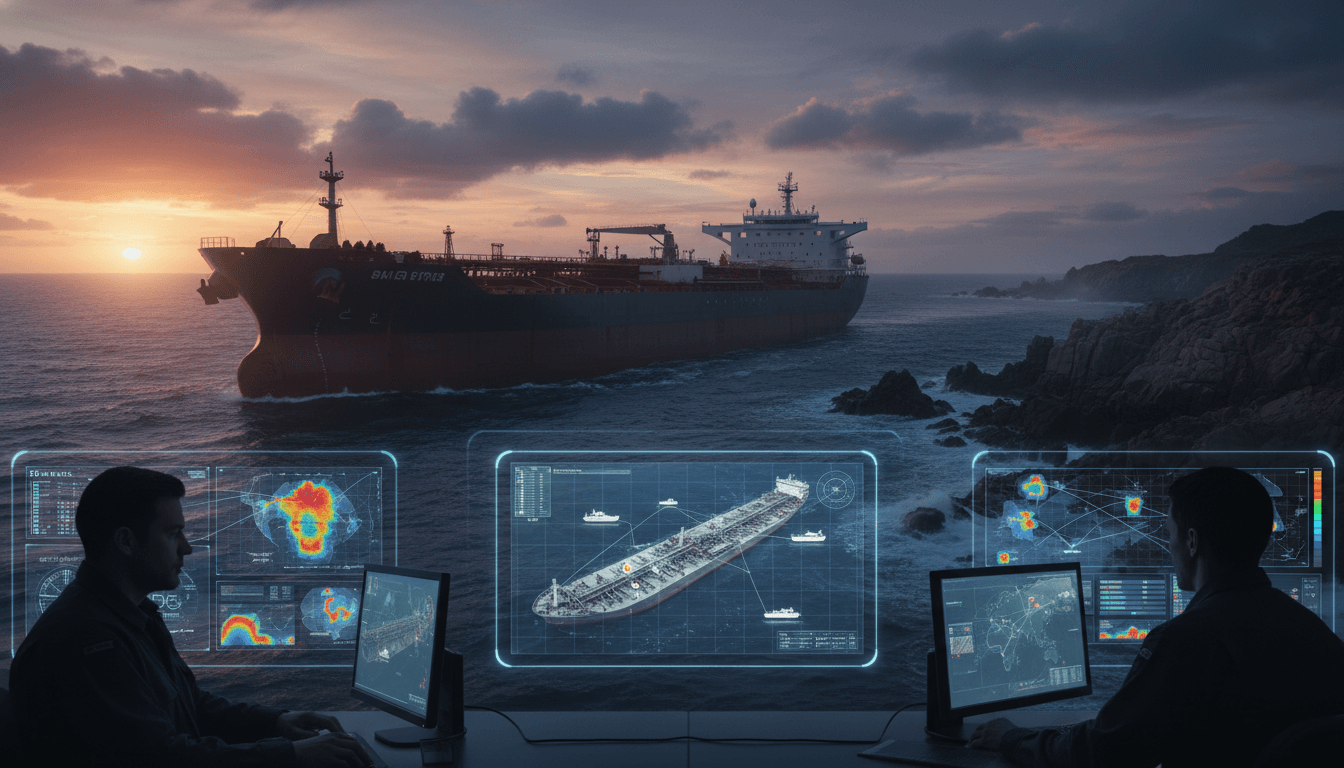

What AI actually does here (beyond “better dashboards”)

AI’s job in this scenario isn’t to “predict war.” It’s to reduce ambiguity and compress decision time.

Well-designed AI systems can fuse multiple signals:

- AIS tracks (including anomaly detection)

- satellite imagery and change detection

- historical route behavior and vessel “fingerprints”

- port call patterns

- weather, sea state, and navigational constraints

- incident feeds and maritime security alerts

Then they can flag what a human team would otherwise miss: behavior that doesn’t match the vessel’s normal operating profile, suspicious gaps, improbable speeds, or sudden corridor clustering.

A simple, quotable way to put it:

In marine war risk, AI doesn’t replace judgment—it makes the facts harder to fake.

How AI improves war risk insurance decisions in real time

The key point: AI enables dynamic risk scoring per voyage, not static pricing per region.

Traditional war risk structures often rely on listed areas and broad geographic ratings. That’s still useful, but it’s too blunt for drone-era threats. Two ships can be in the “same” region with totally different exposure depending on routing, speed, convoying, time of day, and proximity to likely launch areas.

Here’s what AI-driven underwriting can look like in practice.

1) Dynamic voyage risk scoring

Instead of a single rate for “Black Sea transit,” insurers can model a voyage as a sequence of micro-exposures.

A practical scoring model might include:

- route geometry risk (open-water vs coastal track)

- dwell risk (time spent loitering or waiting near choke points)

- proximity risk (distance to past incident clusters)

- anomaly risk (AIS inconsistencies, unusual maneuvers)

- aggregation risk (how many similar vessels are in the same corridor)

Even if you keep human sign-off, AI can produce a consistent baseline so the underwriter isn’t reinventing the wheel each morning.

2) Better pricing discipline when headlines hit

War risk markets can swing sharply after attacks. The danger is overreacting—pricing based on fear rather than measured exposure—then losing business or mispricing the book.

AI helps by separating:

- what changed in incident frequency and severity

- what changed in traffic patterns (like a 70% longer coastal detour)

- what changed in uncertainty (spoofing signals, unknown ownership)

That’s how you avoid “headline pricing” and move toward evidence pricing.

3) Faster claims triage and cleaner investigations

Drone incidents create messy claims files: conflicting coordinates, incomplete logs, and fast-moving political context.

AI can support claims teams by:

- automatically building a timeline of the voyage from multiple data sources

- flagging inconsistencies early (position gaps, suspicious timestamps)

- routing claims to the right specialists based on incident type

It doesn’t eliminate disputes, but it reduces the time wasted chasing basic facts.

What this means for supply chain & procurement teams (not just insurers)

The key point: insurance pricing signals are now supply chain signals.

This post sits in our AI in Supply Chain & Procurement series for a reason: marine war risk isn’t a back-office insurance issue anymore. It’s a procurement and continuity issue.

If you manage energy inputs, chemicals, commodities, or any sea-dependent supply chain, you’re effectively buying a bundle:

- transportation capacity

- route reliability

- geopolitical exposure

- insurance terms embedded in freight economics

A practical playbook: how to use AI signals without building a “moonshot” platform

You don’t need to recreate a maritime intelligence agency. But you do need a repeatable process that turns risk signals into procurement actions.

Here’s what works in the real world:

-

Create a “voyage risk register” for critical lanes

- Track primary routes, alternates, and choke points

- Define what a “material change” looks like (detours, dwell time spikes, AIS gaps)

-

Add risk-adjusted freight planning

- Model scenarios where a detour adds 30–70% distance

- Stress-test inventory buffers and delivery windows

-

Write insurance-aware contract clauses

- Define who pays additional war risk premiums

- Specify notification requirements for route deviations

- Align on evidence standards (AIS, logs, satellite confirmation)

-

Operationalize exceptions

- If AI flags abnormal routing or spoofing patterns, decide in advance:

- do you pause loading?

- require additional guarantees?

- reroute cargo?

- If AI flags abnormal routing or spoofing patterns, decide in advance:

A blunt opinion: most companies wait for a premium spike, then scramble. The better approach is to treat war risk like a variable input cost and manage it continuously.

People also ask: common questions about AI and marine war risk

Does hugging the coast always reduce drone risk?

No. It can reduce exposure to some attack patterns, but it may increase other risks—traffic density, surveillance, navigational hazards, and predictable corridors. The risk profile changes; it doesn’t disappear.

Can insurers rely on AIS data for underwriting and claims?

They can’t rely on it alone. AIS is still valuable, but spoofing and signal gaps mean insurers increasingly need multi-source verification (including satellite imagery and behavioral analytics).

What’s the biggest AI mistake insurers make in geopolitical risk?

Treating AI as a single “risk score” that replaces underwriters. The winning pattern is human decisioning with machine-supported evidence—clear features, explainable triggers, and auditable outputs.

The strategic takeaway: drone-era shipping demands dynamic insurance

The key point: geopolitical volatility is now operational volatility, and AI is how you keep up.

The Black Sea detours are a visible sign of something bigger: supply chains are re-routing in real time to manage kinetic threats, and insurers have to price and manage that reality without guessing.

If you’re a carrier, MGA, broker, or maritime operator, the next step is straightforward: map the data you already have (AIS, claims, incident logs), identify where uncertainty is highest (spoofing, ownership opacity, corridor crowding), and pilot an AI workflow that produces actionable voyage-level decisions.

Where do you see the biggest bottleneck today—getting reliable exposure data, pricing fast enough, or proving what happened when a claim hits?