AI can turn power shutoff alerts into better wildfire risk models, faster claims triage, and clearer customer messaging during outages.

AI for Wildfire Risk When Power Shutoffs Hit

A 60 mph wind forecast can trigger a chain reaction that insurers feel within hours: utilities cut power to reduce ignition risk, customers lose connectivity, alarms go offline, pipes freeze, businesses pause operations, and claims volume spikes—often across multiple lines at once.

That’s exactly the setup parts of Colorado faced this week: Xcel Energy signaled possible preemptive shutoffs across counties that include Denver as warm, dry conditions and strong winds raised wildfire danger. These “public safety power shutoffs” were once mostly associated with California. Now they’re part of how the broader West manages catastrophic wildfire risk.

Here’s the thing most organizations miss: power shutoffs aren’t just an operations issue for utilities—they’re a new input into insurance risk and claims behavior. In the “AI in Energy & Utilities” series, we’ve been tracking how data from the grid is becoming as important as data from the sky. This post focuses on what insurers can do—practically—using AI to anticipate loss, triage claims, and communicate better when the lights go out.

Power shutoffs are becoming a wildfire risk signal

Power shutoffs are a measurable, forecastable indicator of elevated wildfire conditions—and insurers should treat them like a risk alert, not a news headline. When a utility prepares to de-energize lines, it’s reacting to a specific combination of variables: wind gusts, fuel dryness, humidity, terrain, and equipment exposure.

In the Rockies scenario, forecasters expected gusts up to about 60 mph, which is high enough to move branches into lines, shake hardware loose, and increase the chance of downed conductors. Utilities choose shutoffs because the alternative is worse: a single spark in the wrong corridor can turn into a community-scale loss in hours.

Why this matters for insurance portfolios

Insurers often model wildfire hazard using vegetation, topography, historical fire perimeters, and weather. That’s necessary—but incomplete. A utility shutoff plan is an operational decision that encodes “real-world risk” in a way actuarial tables can’t.

When you ingest shutoff probability (or even a “watch” status) into underwriting and claims readiness, you get earlier and more accurate answers to questions like:

- Which ZIP codes are most likely to experience service interruption?

- Which insured properties have higher secondary-loss exposure (pipes freezing, sump pumps failing, security systems down)?

- Which commercial insureds are at risk of business interruption due to outage-dependent operations?

The under-discussed loss driver: secondary damage

Wildfire is the headline peril, but shutoffs create secondary loss pathways that swell claim counts:

- Frozen pipe and water damage when heat systems fail during cold snaps (very relevant in December)

- Food spoilage for homeowners and small businesses

- Security and vandalism claims when alarms and cameras lose power

- HVAC and equipment issues from abrupt shutdowns or generator misconfiguration

A strong AI program doesn’t just predict “fire or no fire.” It predicts which losses are likely even if no wildfire occurs.

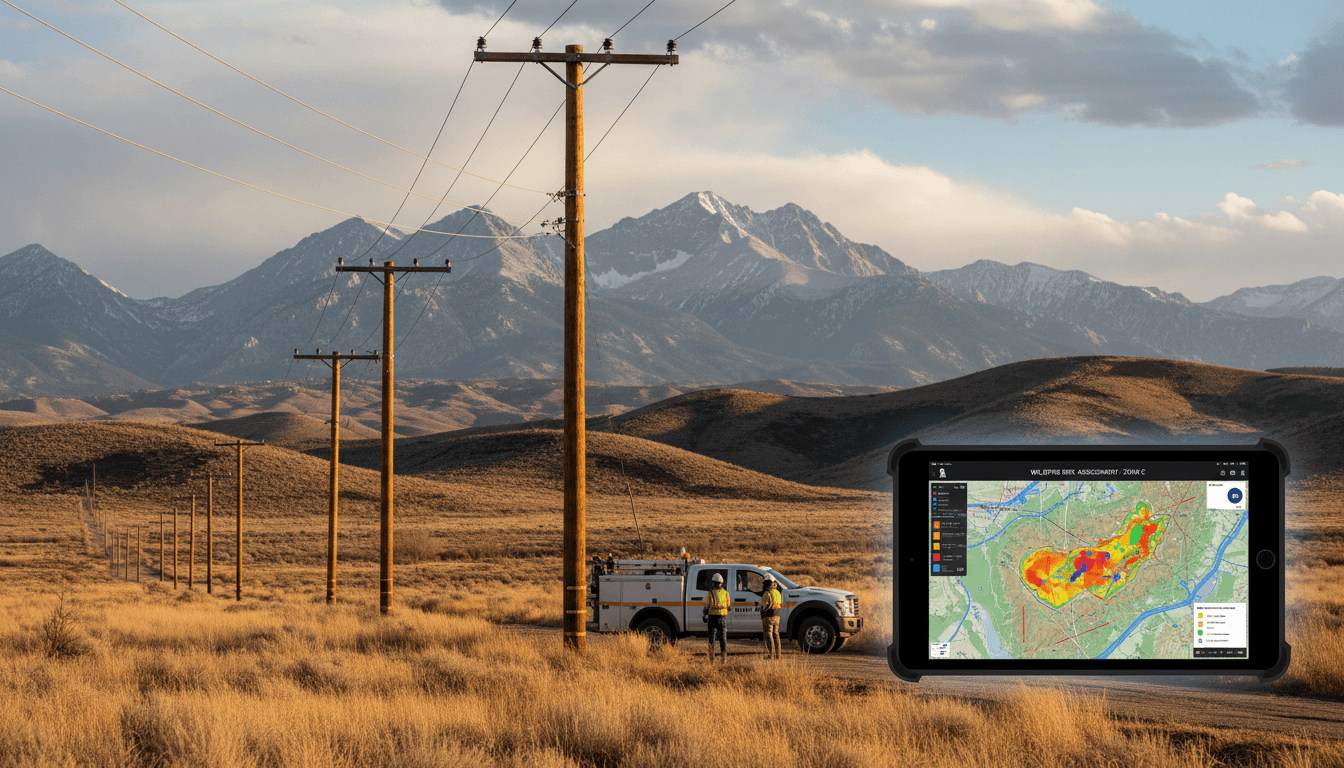

How AI improves wildfire risk modeling with grid + weather data

The fastest way to improve wildfire risk modeling is to combine real-time weather forecasts with utility operations and asset exposure data. If you’re only looking at weather, you’re missing the operational trigger that changes the risk landscape.

The goal is a model that can answer: Given this wind forecast and shutoff footprint, what’s the expected loss across my book in the next 72 hours?

What data to fuse (and what to do with it)

A practical “AI for wildfire risk” stack usually blends:

- Weather: wind gust forecasts, humidity, temperature anomalies, red-flag conditions

- Vegetation and fuels: dryness indicators, land cover, seasonal fuel loading

- Topography: slope, aspect, canyon/wind corridor effects

- Utility operations: shutoff advisories, restoration estimates, feeder-level risk where available

- Exposure: property characteristics, construction type, defensible space proxies, proximity to WUI

- Behavioral signals: call center volume, app logins, policyholder location patterns (where privacy allows)

Then apply AI in two layers:

- Hazard nowcasting (short-horizon risk): forecast ignition and spread probability at fine spatial resolution.

- Loss translation (insurance impact): convert hazard + outage context into expected claims by line, severity bands, and staffing needs.

A stance: “more data” isn’t the win—better labeling is

I’ve found the biggest lift doesn’t come from adding yet another dataset. It comes from labeling outcomes correctly:

- Separate wildfire claims from outage-driven claims.

- Tag claims by trigger conditions (wind threshold, outage duration, restoration delays).

- Capture property-level mitigation signals (roof type, vents, defensible space) in structured form.

When you do that, models stop being vague “risk scores” and become operational tools.

Claims automation that still works when disasters disrupt operations

During weather-driven events, claims performance is mostly a throughput problem—intake, triage, and decisioning get overloaded. Preemptive shutoffs add another constraint: customers may have limited connectivity, and adjusters may face access issues.

This is where AI earns its keep, not as a shiny add-on, but as a way to keep service levels stable.

AI triage: get to the right claim first

Instead of first-come, first-served, modern catastrophe workflows prioritize based on severity likelihood and urgency.

A solid AI triage approach can:

- Classify FNOL narratives into likely perils (fire, smoke, frozen pipe, spoilage)

- Detect “time-critical” claims (active water leak, displaced families, vulnerable insureds)

- Recommend next-best action (self-service guidance, emergency vendor dispatch, desk adjuster, field inspection)

One important operational detail: triage models should be retrained on catastrophe language. People describe wind and smoke differently under stress. The model needs to handle messy inputs.

Document and photo automation (without punishing customers)

If customers have intermittent power or cellular service, they may upload fewer photos or incomplete forms. AI should adapt:

- Accept partial submissions and prompt for only what’s missing

- Use computer vision to estimate damage from fewer images (with clear confidence thresholds)

- Route low-confidence cases to humans quickly

The point isn’t to minimize human involvement. It’s to use humans where judgment is actually needed.

Restoring power can take days—plan claims comms accordingly

Utilities often can’t re-energize lines until crews inspect and repair damage. That means outages can extend beyond the worst wind window.

Claims teams should assume:

- Higher call volume after weather improves (when customers can finally report)

- Increased vendor demand for water mitigation and temporary housing

- Elevated risk of fraud attempts in the confusion (AI anomaly detection helps here)

AI-powered customer engagement during emergency shutoffs

When power shutoffs hit, customers don’t want generic catastrophe pages. They want specific, local, actionable guidance. AI can deliver that at scale.

What “good” looks like for policyholder communication

Effective engagement isn’t more messages—it’s better timing and better targeting:

- Send outage-specific tips to impacted ZIP codes (generators, frozen pipe prevention, food safety)

- Provide short claim checklists that fit on a phone screen

- Offer bilingual support automatically based on prior preferences

- Use chat or voice bots for triage, with a fast path to a human for urgent situations

A line I use internally: Every unclear message becomes a claim expense. Confusion drives repeat contacts, delays mitigation, and increases loss severity.

Proactive mitigation: reduce losses before they happen

Insurers can reduce both loss and frustration by using AI to trigger prevention outreach when shutoff risk rises:

- “If your heat relies on electricity, shut off and drain exposed pipes” guidance

- “Test your sump pump backup” reminders

- “Charge medical devices and confirm backup plans” for at-risk households

This isn’t just goodwill. It’s loss control with measurable ROI.

What insurance leaders should do before the next wind event

The organizations that handle wildfire and shutoff events well treat them like planned surges. Wind forecasts give you lead time. Shutoff advisories give you geographic precision.

A practical 30-day blueprint

If you’re building (or tightening) your AI approach to wildfire risk and outage events, focus on these moves:

-

Create a shutoff-aware exposure view

- Map policies to utility territories and likely shutoff footprints.

- Identify clusters with high business interruption sensitivity.

-

Build a “secondary loss” playbook

- Pre-script guidance for frozen pipe prevention, food spoilage, and security concerns.

- Align endorsements and coverage explanations with plain-language templates.

-

Stand up catastrophe-grade intake and triage

- Add surge capacity for digital FNOL.

- Use AI routing to prioritize urgent losses.

-

Pre-arrange vendor capacity

- Water mitigation, debris removal, temporary housing, generator servicing.

- Use AI demand forecasting to allocate vendors by geography.

-

Instrument your outcomes

- Track cycle time, customer contacts per claim, severity drift, and reopening rates.

- Feed those metrics back into models.

“People also ask” questions you should be ready to answer

Do power shutoffs reduce wildfire losses overall? Yes, they’re designed to reduce ignition risk from electrical equipment during extreme conditions. But they can increase non-fire claims like frozen pipes and spoilage.

Can AI actually predict claim volume from wind and outage forecasts? Yes—especially at the portfolio level—when you combine weather, exposure, and historical claim outcomes tied to similar events.

What’s the biggest mistake insurers make during outages? Treating every claim the same. A frozen pipe active leak and a spoiled fridge claim shouldn’t move through the same workflow.

Where this is heading for AI in Energy & Utilities

Utilities are increasingly using AI for grid optimization, outage prediction, and vegetation management. Insurers are increasingly using AI for risk modeling and claims automation. The next step is obvious: shared situational awareness. Not sharing customer data—sharing hazard context, outage footprints, and restoration expectations so both industries can act faster.

Power shutoffs in places like Denver aren’t a one-off. They’re a new normal response to extreme wind and fire weather. Insurers that integrate utility and weather signals into AI workflows will price risk more accurately, serve customers faster, and reduce avoidable secondary losses.

If you’re planning for 2026, here’s the question to pressure-test your program: When the next shutoff notice hits at 10 a.m., can your organization translate that into action by noon—underwriting, claims, vendors, and customer messaging—without chaos?