Wildfire liability is shifting toward negligence. See how AI improves utility risk controls, underwriting, and claims defensibility after the Texas-Xcel lawsuit.

AI for Wildfire Liability: Lessons from the Xcel Case

Wildfire liability has a new face in Texas: a state lawsuit accusing a major utility of “blatant negligence” tied to a deadly blaze with more than $1 billion in damage and three fatalities. In the complaint, Texas seeks punitive damages, consumer restitution, and even a court order that could force immediate replacement of utility poles—plus an attempt to block the utility from passing costs to customers through rate hikes.

Here’s what I keep coming back to: this isn’t only a legal story. It’s a data story. The allegations—aging infrastructure, ignored warnings, poor disclosure, and a mismatch between public safety messaging and operational reality—are exactly the kinds of gaps that AI systems can surface early, measure continuously, and help govern.

This post is part of our “AI in Energy & Utilities” series, where we look at how utilities, insurers, and risk teams are using AI for grid optimization, predictive maintenance, and extreme weather resilience. The Texas-Xcel case is a clean case study for a messy reality: wildfire risk has become an enterprise-level liability problem, and AI is quickly becoming the toolset that separates “we didn’t know” from “you should’ve known.”

What the Texas-Xcel lawsuit signals for risk and insurance

The big signal is simple: wildfire exposure is moving from “catastrophe risk” to “operational negligence risk.” That change matters because catastrophe losses are typically treated as external events; negligence claims are about internal decisions, controls, and evidence.

In the Texas lawsuit, the state alleges the utility misrepresented safety commitments, ignored warnings about infrastructure needing repair, and failed to disclose hazards—while the utility disputes negligence and points to an expedited claims fund that reportedly paid $361 million so far. Regardless of who prevails, the direction of travel is clear: utilities will be judged on what they monitored, what they predicted, what they warned, and what they fixed.

For insurers and reinsurers, this pushes wildfire underwriting and claims into a new zone:

- Liability limits and exclusions get tested, not just property coverage.

- Subrogation becomes central: insurers will pursue recovery if they believe a utility’s equipment ignited the loss.

- Claims handling becomes more documentation-heavy: causation timelines, equipment maintenance records, vegetation management logs, weather data, and customer communications.

When a state starts asking for court-ordered infrastructure replacement and restrictions on rate recovery, it’s also telling the market something else: regulatory and legal risk is now part of the wildfire model.

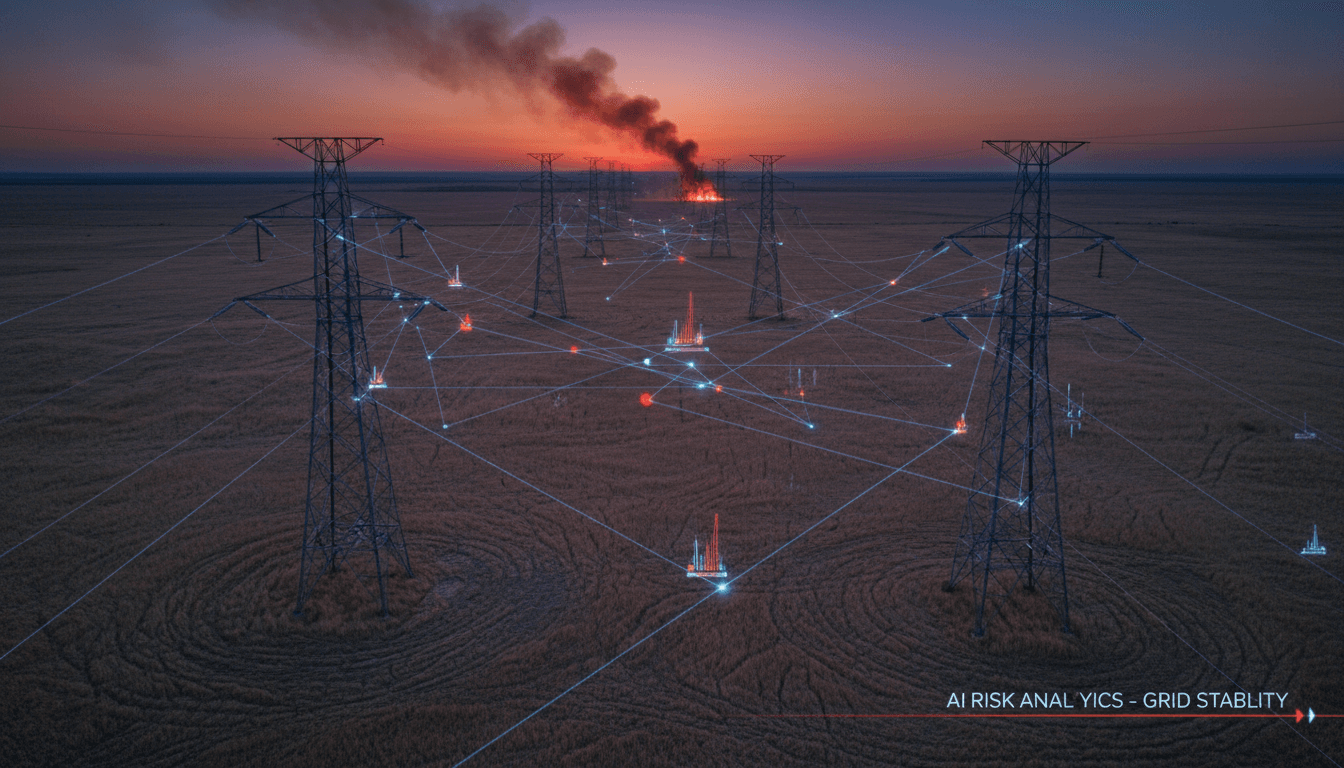

AI wildfire risk assessment: what “good” looks like in 2026

AI wildfire risk assessment works when it behaves less like a one-time score and more like a living system that updates daily (or hourly) as conditions change. The best implementations connect three layers: environment, grid assets, and human decisions.

Layer 1: Environmental ignition and spread forecasting

AI models can combine near-real-time inputs—wind, humidity, vegetation dryness proxies, topography, and historical burn patterns—to generate dynamic ignition likelihood and spread severity forecasts.

What’s different from older catastrophe modeling is cadence and granularity. Traditional models often support annual pricing and portfolio management. Operational AI supports tomorrow’s dispatch plan.

Practical outputs utilities and insurers can actually use:

- Feeder-level risk maps (which circuits are most dangerous right now)

- Time-window alerts (risk spikes between 1–6 pm due to winds)

- Scenario spread cones (where a fire could travel given forecast winds)

Layer 2: Asset condition, failure probability, and “weak signals”

Most companies get this wrong by treating asset health as a maintenance spreadsheet problem. It isn’t. Asset health is a probabilistic forecasting problem.

AI-driven predictive maintenance can estimate failure likelihood for poles, conductors, insulators, transformers, and reclosers by combining:

- age and material type

- inspection images (computer vision)

- infrared/thermal anomalies

- outage history and near-miss events

- vegetation proximity and encroachment rates

This matters because lawsuits hinge on foreseeability. If internal data shows repeated anomalies on a line segment during high-risk conditions, and the utility doesn’t act, that’s not “bad luck.” That’s discoverable.

Layer 3: Decision intelligence (who did what, when, and why)

Wildfire litigation and claims don’t only ask, “Did equipment start a fire?” They ask, “Were controls reasonable?”

Decision intelligence is where AI helps an organization prove it had a disciplined process:

- risk thresholds for public safety power shutoffs (PSPS)

- documented exceptions when power stays on

- automated customer alerts when risk exceeds thresholds

- work-order prioritization tied to quantified risk

A strong posture is auditable: the model output, the decision, and the reason are captured in a single chain of evidence.

AI in insurance: pricing and claims when negligence is on the table

For insurers, AI adds value in two places where wildfire cases get expensive fast: underwriting and claims.

Underwriting: from static territory factors to asset-aware pricing

When wildfire liability becomes a recurring issue, insurers need pricing that reflects more than zip codes and brush maps. The underwriting question becomes:

“How does this operator behave under stress, and what do their assets look like up close?”

AI can help carriers move toward operator-informed risk pricing by scoring:

- inspection frequency and completeness (including image coverage)

- backlog of critical maintenance

- vegetation management cycle times

- PSPS governance maturity

- incident response performance (time to de-energize, time to notify)

The result isn’t just a premium change. It’s a clearer view of who is “investable” from a risk standpoint.

Claims: faster triage, better documentation, smarter recovery

Wildfire claims are multi-party, multi-coverage, and politically sensitive. AI helps by:

- Automating intake and triage (classifying loss types, severity, and needed adjuster skills)

- Extracting documentation from photos, invoices, and repair estimates

- Building event timelines (weather + outage logs + dispatch notes + customer communications)

- Subrogation targeting (identifying likely responsible parties based on ignition zone and equipment proximity)

If you’re a claims leader, here’s the blunt truth: the winners in wildfire claims will be the teams that can assemble a defensible timeline in days, not months. AI is how you do that at scale.

The overlooked part: consumer protection, disclosure, and “truth in risk”

One of the sharper elements in the Texas complaint is the consumer protection angle: alleged misrepresentations about safety and reliability, and failure to disclose hazards.

That should worry every high-risk infrastructure operator because disclosure is becoming a second battlefield—separate from ignition causation.

AI can support “truth in risk” in a practical, defensible way:

- Customer-facing risk notifications triggered by objective thresholds

- Public dashboards that show PSPS criteria and status (without exposing sensitive security details)

- Consistent messaging generated from a controlled risk taxonomy (so teams don’t freelance language)

This isn’t marketing. It’s liability hygiene.

A utility’s credibility is an asset. Once it’s gone, every future incident gets priced like negligence.

An AI playbook for utilities and insurers (the parts that actually reduce loss)

A lot of AI talk stays abstract. Here’s a concrete playbook I’ve seen work—focused on measurable risk reduction and better defensibility.

1) Start with a “risk register” that models can update

Treat wildfire like a living risk register. Each circuit, segment, and asset class gets:

- a baseline risk score

- a seasonal adjustment factor

- an operational posture (inspection cadence, vegetation status, open work orders)

The model’s job is to keep that register current.

2) Make predictive maintenance prioritization non-negotiable

Most maintenance backlogs are “first in, first out” with political overrides. Change that.

A workable rule is:

- Risk-weighted work orders: highest wildfire consequence × highest failure probability goes first

- Documented exceptions only (with named approver)

3) Build PSPS governance that can survive discovery

Whether or not PSPS is used, governance needs to be clear:

- threshold definitions (wind, humidity, fuel dryness proxies)

- circuit-specific exceptions (critical facilities)

- escalation procedures

- evidence capture (model output, decision, notification logs)

4) Create a joint utility–insurer “loss prevention loop”

The fastest maturity jump happens when insurers stop being periodic auditors and become partners in measurable mitigation.

Examples of shared metrics:

- reduction in high-risk line miles without completed inspections

- time-to-close critical maintenance work orders

- vegetation clearance compliance rates

- incident near-miss reporting volume (higher can be better early on)

5) Prepare your “first 72 hours” claims and comms protocol

If a fire happens, the first 72 hours will define litigation posture for years.

AI-ready organizations have:

- automated data retention and legal hold triggers

- pre-built event timeline templates

- approved language for public safety updates

- claims triage models pre-trained on past catastrophe events

Practical Q&A insurers and utilities are asking right now

Can AI actually prevent utility-caused wildfires?

AI prevents fires indirectly by making failure more predictable and mitigation more consistent. The prevention comes from acting on the model: targeted maintenance, better vegetation management, and disciplined operational shutoff decisions.

Does using AI increase liability if the model flags risk and you don’t act?

Yes. If an organization deploys risk models and ignores them, it can create a “you knew” problem. The solution is governance: clear thresholds, documented decisions, and a credible mitigation plan tied to outputs.

What’s the first AI investment with the highest ROI?

In wildfire regions, it’s typically asset condition analytics + risk-weighted maintenance prioritization. It reduces both ignition probability and negligence exposure because it’s tangible, documentable action.

Where this is heading in 2026: “operational proof” becomes part of coverage

Wildfire litigation like the Texas-Xcel case is pushing the industry toward a future where insurance and regulation both demand operational proof:

- Proof that inspections happened

- Proof that hazards were quantified

- Proof that the organization acted proportionately

- Proof that customers were warned consistently

AI is the practical way to generate that proof without drowning teams in manual reporting.

If you’re a utility, the goal isn’t to sound committed to safety—it’s to show your work. If you’re an insurer, the goal isn’t to guess at wildfire exposure—it’s to price the operator, not just the territory.

Wildfire risk isn’t getting easier, and legal scrutiny isn’t getting softer. The question is whether your data and decisions will look disciplined when someone else tells the story.