Remittances-first is a trust strategy. Learn what Nomba’s DRC expansion teaches Ghana about AI, mobile money, agents, and fintech growth.

Remittances First: AI Fintech Lessons for Ghana

A market where 80%+ of adults have never held a bank account forces fintechs to win differently: not with fancy features, but with trust, cash logistics, and daily usefulness. That’s the reality in the Democratic Republic of the Congo (DRC)—and it’s why Nomba, a Nigerian fintech last valued at $150 million+, is entering the DRC through one product most people already rely on: remittances.

This post sits inside our series “AI ne Fintech: Sɛnea Akɔntabuo ne Mobile Money Rehyɛ Ghana den”—how AI is strengthening accounting, mobile money, and fintech operations in Ghana through automation and trust-building. The DRC story matters for Ghana because the core constraint is similar: people may use mobile money, but they don’t automatically trust digital finance enough to keep value in it.

Nomba’s approach—start with where money already moves, build physical distribution, then layer on payments and credit—offers a practical playbook for Ghanaian fintechs, aggregators, and mobile money businesses. The extra ingredient Ghana can add is AI-driven operations: smarter fraud controls, better agent liquidity planning, faster onboarding, and more reliable customer support.

Why remittances are the fastest way to “borrow trust”

Remittances work as an entry point because they’re already a habit, not a new behavior to sell. In the DRC, remittance inflows from high-volume corridors like China and Dubai power traders and small businesses. Nomba is recruiting physical agents to handle these flows, aiming to earn “transactional trust” first.

Here’s the insight Ghana should steal: trust is built when money arrives on time, every time, with no drama. Not when an app has 40 features.

In cash-heavy environments, the customer’s mental model is simple:

- “If I can cash out quickly, this service is real.”

- “If I can find an agent easily, this service is dependable.”

- “If rates and fees don’t surprise me, this service is fair.”

Ghana already has stronger digital rails than the DRC in many respects, but the trust math is the same—especially for cross-border flows (diaspora remittances), SME collections, and informal trader payments.

What “remittances first” really means for Ghana

For Ghanaian fintech operators, “remittances first” doesn’t have to mean becoming a remittance company. It means:

- Start with a high-frequency, high-need transaction (salary advances, merchant collections, school fees, diaspora top-ups, utility payments).

- Attach reliability guarantees (clear settlement times, transparent fees, dispute handling).

- Turn those repeat transactions into a profile that supports savings, working capital, and bookkeeping.

That last step is where AI becomes more than hype—it becomes operations.

The real competition isn’t another app. It’s cash.

The DRC is still mobile-money-driven, but mostly for cash-in/cash-out. Many users withdraw immediately after receiving funds. That pattern is familiar across cash-dominant ecosystems: digital wallets are treated like pipes, not vaults.

In the DRC, mobile money operators reportedly hold 24 million+ wallets, yet the everyday value often ends at withdrawal. Meanwhile, banks focus on government, mining, and donor-driven flows—leaving daily commerce underserved.

Ghana is ahead on wallet usage, merchant payments, and interoperability—but cash still has three advantages:

- Instant finality: no reversal anxiety.

- Universal acceptance: no “network is down” excuse.

- Privacy by default: no one asks questions.

So if you’re building fintech in Ghana, your product is competing with a currency note that has had decades to earn trust.

How AI helps compete with cash (without fighting customers)

I’m opinionated here: fintechs lose when they try to force users to “go cashless.” They win when they reduce the reasons people run back to cash.

AI helps by making digital money behave more like cash on the things people care about:

- Speed: AI-assisted routing can reduce failed transfers by choosing the best rail or fallback path.

- Certainty: ML-based risk scoring can enable instant approval for low-risk transactions while holding suspicious ones.

- Support: AI customer service can resolve common issues (wrong wallet, pending cash-out, charge disputes) in minutes, not days.

If digital reliability becomes boringly consistent, keeping value in the wallet stops feeling risky.

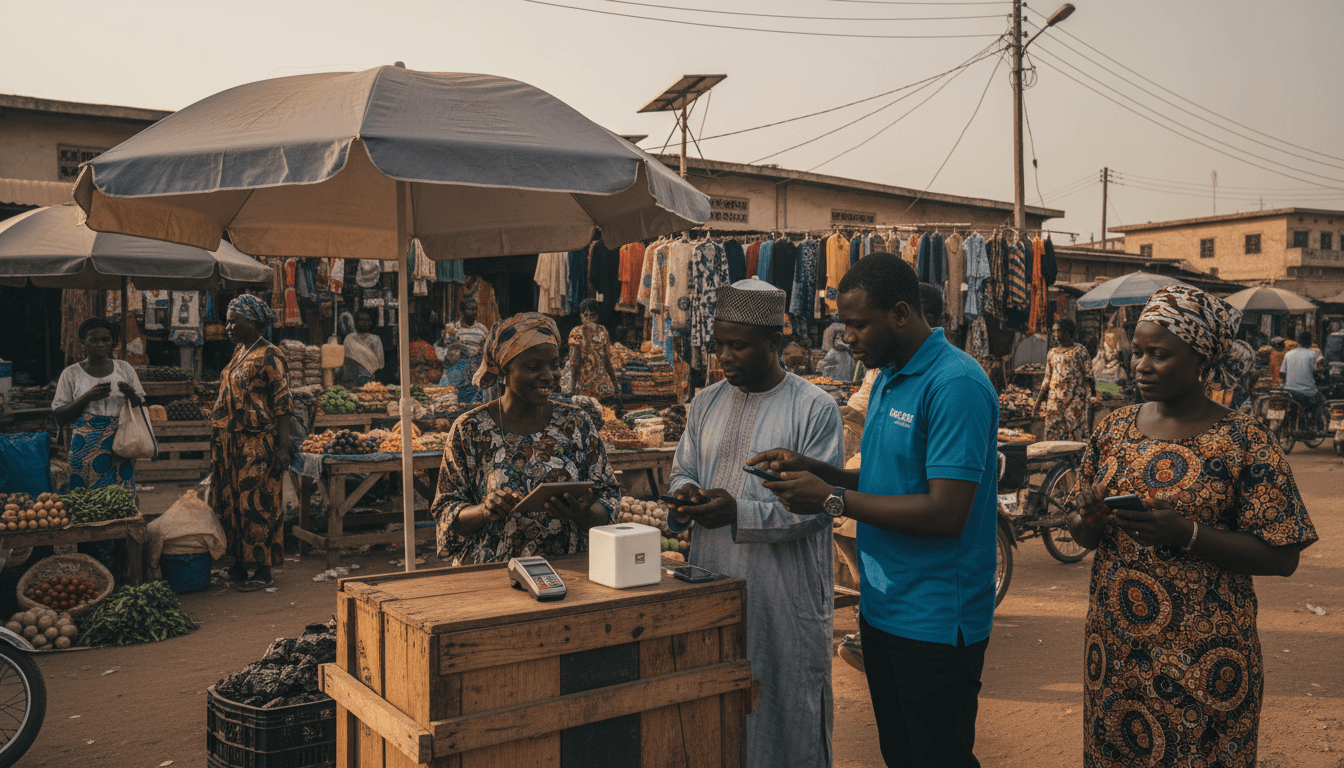

Agent networks: the unglamorous infrastructure that decides growth

Nomba’s DRC strategy depends heavily on physical agents—because in-person assurance is still how many users evaluate legitimacy. Their country manager notes that unlike Nigeria, where you can onboard online without meeting anyone, DRC customers often want face-to-face confidence.

Ghana’s agent ecosystem is larger and more mature, but the same physics applies:

- If agents don’t have liquidity, customers blame the fintech.

- If agents churn, coverage collapses.

- If settlement is slow, agent float becomes expensive.

One DRC-specific challenge Nomba highlights is slow bank settlement times, which worsens liquidity management. Ghana faces its own versions: peak-hour downtime, reconciliation delays, chargeback disputes, and agent float stress during holidays.

AI for agent liquidity and reliability (practical use cases)

This is where AI in mobile money operations moves from buzzword to profit line. A few high-impact applications:

-

Float prediction by location and day

Models can forecast cash-in/cash-out demand per agent zone using seasonality (month-end), events (Christmas/New Year), and local market days. -

Early-warning signals for agent churn

Detect patterns like falling transaction volume, increasing complaints, or repeated settlement issues—then intervene with targeted incentives. -

Fraud and collusion detection

Identify suspicious agent-user networks, abnormal reversal patterns, or transaction splitting designed to evade limits. -

Automated reconciliation

Use anomaly detection to flag mismatches between ledger entries, bank settlements, and agent balances before they become expensive disputes.

For Ghanaian fintechs and aggregators, these aren’t “nice-to-haves.” They’re the difference between growth that’s controllable and growth that breaks.

Snippet-worthy truth: In cash-heavy markets, your agent network isn’t a channel. It’s your product.

Regulation and compliance: AI makes “growth with control” realistic

Nomba entered the DRC by partnering with banks and aligning with local KYC, transaction monitoring, and AML expectations. The DRC central bank (BCC) is described as friendly toward digitisation, but the system is still high-risk because cash dominance creates more room for laundering and fraud.

Ghana’s compliance environment is also tightening across fintech and mobile money—especially around onboarding quality, fraud prevention, and transaction monitoring. The trade-off is familiar: stricter controls can slow growth unless you automate.

What AI can automate responsibly (without breaking trust)

AI is most useful when it reduces friction for legitimate customers while raising the bar for bad actors. Examples that work well in practice:

- Intelligent KYC checks: document verification, selfie matching, duplicate detection, and name similarity checks.

- Risk-based transaction limits: dynamic caps that expand as trust signals grow (consistent inflows, stable device, verified merchant activity).

- Behavioral monitoring: flag unusual activity (new device + high amount + rapid cash-out) for step-up verification.

The goal isn’t surveillance. It’s predictability: fewer sudden account freezes for honest users, and fewer open doors for fraud rings.

The “layering” strategy: build rails, then add payments and credit

Nomba’s plan is clear: remittances → payments rails → additional products (collections, credit). That sequencing is smart because it matches how trust accumulates.

Credit, especially, is a trust product. In cash-heavy economies, lending fails when repayment is inconvenient or when scoring is disconnected from real cashflow.

Ghana-specific opportunity: AI-powered credit tied to real cashflow

Ghana has a huge advantage: mobile money and merchant payment data can become cashflow evidence for SMEs who don’t keep formal books.

A strong approach looks like this:

- Start with collections (merchant receives wallet payments, invoice collections, QR payments, USSD checkout).

- Auto-generate simple bookkeeping (daily sales, refunds, customer concentration, seasonal trends).

- Offer working capital based on observed cashflow, with repayment linked to future receipts.

If you’re running an SME, this is where AI becomes personal: it can turn “I don’t have accounts” into “my transactions are my accounts.” That’s exactly the theme of this series—AI ne fintech reboa akɔntabuo ne mobile money so businesses can grow without drowning in paperwork.

People also ask: what should Ghanaian fintechs copy—and what should they avoid?

Should a Ghanaian fintech also start with remittances?

If you have distribution and compliance capacity, yes—remittances are a powerful trust engine. If not, copy the principle instead: start with a transaction customers already do weekly.

Is an agent-first strategy still necessary in Ghana?

For mass adoption outside affluent urban clusters, yes. Digital onboarding helps, but human touchpoints reduce fear, especially for first-time users and SMEs handling larger sums.

Where does AI actually pay for itself?

AI pays fastest in:

- fraud reduction (loss prevention)

- automated support (lower cost-to-serve)

- agent liquidity planning (higher uptime and transaction completion)

- credit risk (lower defaults)

If an AI project doesn’t move one of those, treat it as a lab experiment—not a priority.

What to do next (if you’re building fintech or running a business)

Nomba’s DRC move is a reminder that distribution + trust beats features in cash-heavy markets. Ghana’s ecosystem is more mature, but the same constraints show up in different clothing: agent liquidity, fraud, onboarding friction, and the gap between wallet usage and deeper financial services.

Here’s a practical next step, depending on who you are:

- Fintech founders/operators: audit your “trust pipeline” (onboarding → first transaction → support → dispute resolution). Add AI where it reduces failure rates, not where it looks impressive.

- Mobile money agents/aggregators: use data to manage float and staffing for end-of-month and holiday peaks. AI forecasting is cheaper than losing customers due to “no cash.”

- SMEs and traders: prioritize payment methods that also generate records. The fastest route to affordable credit is a reliable cashflow trail.

The broader series question remains: Sɛnea AI ne fintech bɛma Ghana ayɛ den? My stance: Ghana wins when AI is used to make digital finance more dependable than cash—quietly, consistently, and at scale. What part of your customer journey still breaks trust today: onboarding, cash-out, support, or disputes?