AI fintech ne mobile money betumi ama crisis payments ayɛ ntɛm, transparent, na ɛfa wɔn a ɛhia wɔn no so. Hwɛ practical blueprint ama Ghana 2026.

AI Fintech ne Mobile Money: Sikasɛm Mmoa a Ɛda mu

4.6 million nnipa wɔ Somalia na osu-asen (drought) aka wɔn—na sika a wɔde boa wɔn no nso resi so tua (funding shortfalls). Wɔde $1.4 billion hyɛɛ 2025 response plan mu, nanso sika a aba mu yɛ bɔɔkɔɔ: bɛyɛ $370 million pɛ. Sɛ wode saa nɔma yi bɔ mu a, wuhu amanehunu no: wɔwɔ adwuma a wɔpɛ sɛ wɔyɛ, nanso sika no ntumi nnya kwan mmra ntɛm, nntumi nntena hɔ, na nntumi nnkɔ ɔkwan a ɛfata so.

Ɛnyɛ Somalia nkutoo. Sudan ko no rekɔ “catastrophic levels” bere a ɛbɛn nna 1,000 (bɛyɛ mfeɛ mmiɛnsa) mu no, na nkitahodie a ɛma mmoa du nnipa so no asɛe wɔ mmeae bi. Saa bere yi mu—December 2025, a ɛyɛ Ghana “December tourism” (wɔpɛ sɛ wɔsan rebrand a ɛnyɛ “Detty December”)—sika kɔɔ so, nnipa tu baa Ghana, na mobile money transactions no taa sɔre. Ɛyɛ bere pa a yɛbɛka asɛm bi a Ghana ne Africa nyinaa hia: sɛ yebetumi de AI-driven fintech ne mobile money ayɛ mmoa, a ɛyɛ transparent, ntɛm, na ɛma sika du wɔn a ɛhia wɔn no so a, yɛbɛtumi atew amanehunu mu.

Saa post yi wɔ “AI ne Fintech: Sɛnea Akɔntabuo ne Mobile Money Rehyɛ Ghana den” series no mu. M’ani si so sɛ yɛbɛfa Somalia osu-asen ne Sudan ko ho nsɛm yi ayɛ practical lessons ama Ghana’s fintech, NGOs, ne businesses—sɛnea wɔn bɛyɛ sika ho nhyehyɛe pa, wɔn de automation ayɛ adwuma, na wɔn de data ne AI ama accountability ayɛ den.

Adɛn nti na funding shortfalls no da fintech ho mmerɛw adi

Sɛ mmoa sika sua a, asɛm no nnyina “sika nni hɔ” nkutoo. Ɛtaa yɛ sika no duru (distribution friction): bank transfers a ɛgye bere, cash logistics a ɛyɛ risk, duplication (nnipa bi nya mmoa mmienu, na afoforo nnya), ne corruption a ɛma confidence tu.

Somalia report no kyerɛe nsɛm a ɛwɔ “human outcomes” mu pɛ:

- 4.6 million nnipa aka osu-asen no mu (bɛyɛ 1/4 population)

- 120,000 nnipa atu fi September–December

- 75,000 sukuu mmɔfra agyae sukuu

- Dry season January–March bɛtumi ama tebea no nyɛ den kɛse

Fintech lesson: Sɛ sika no sua a, na “waste” biara yɛ asɛe. Saa nti transparency, automation, ne targeting (ɔhene mu: wɔn a ɛhia wɔn paa) no nyɛ luxury—ɛyɛ survival.

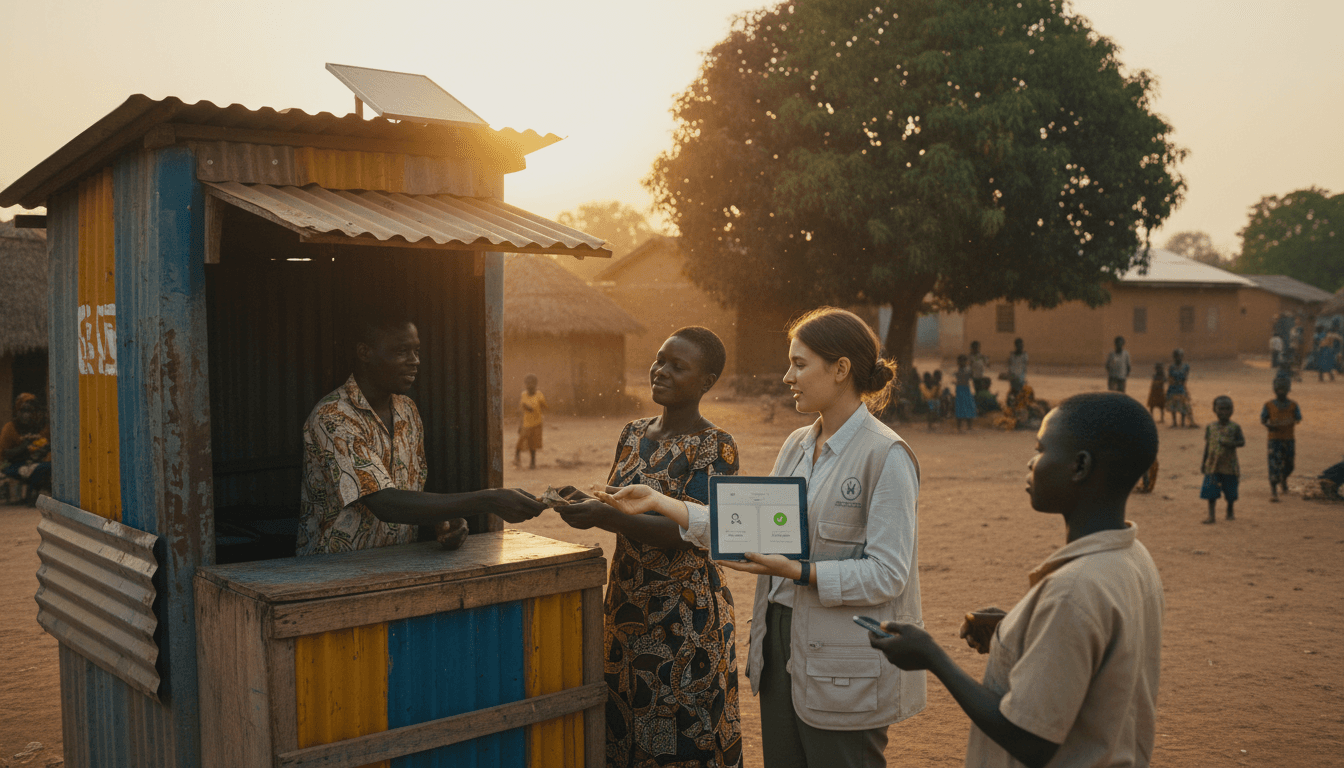

Sɛnea mobile money boa ma cash aid yɛ adwuma

Mobile money ma “cash assistance” kɔ beneficiary so ntɛm. Nanso sɛnea m’ahunu wɔ projects bi mu no, mobile money ankasa ntumi nsi problem no nyinaa:

- beneficiary verification (KYC) betumi ayɛ den

- SIM swaps ne fraud betumi asɛe mmoa

- agent liquidity betumi ama nnipa nntumi nnya cash (sɛ ɛhia)

- data fragmentation (NGO, telco, bank, government) ma auditing yɛ dɛnn

Ɛha na AI fintech bɛtumi akɔ soro.

AI fintech: mfasoɔ a ɛteɛ, ɛnyɛ buzzwords

AI fintech bɔ mmɔden wɔ nneɛma mmiɛnsa: (1) detection, (2) decisioning, (3) delivery.

1) Detection: hunu hena na ɔhia mmoa, na bere bɛn

Crisis mu no, target accuracy yɛ ade titiriw. AI betumi aboa wɔ:

- Risk scoring (area drought severity, food price spikes, displacement patterns)

- Household vulnerability models (family size, school dropout signals, livestock loss proxies)

- Early warning triggers (e.g., water price rising for 3 weeks + market shortages)

Sɛ Ghana rehwehwɛ social protection ne disaster response mu (floods, drought pockets, inflation shocks), model a ɛte saa no bɛtumi aka LEAP payments, NADMO support, ne district-level emergency funds ho.

2) Decisioning: si gyinae ntɛm—nanso fa rules a ɛda mu so

AI nkyerɛ sɛ “computer na ɛyɛ adwuma nyinaa.” Best practice ne rules + AI:

- Rules: eligibility criteria a ɛda mu (e.g., pregnant mothers, disabled persons, households in declared emergency zones)

- AI: prioritize, detect anomalies, reduce duplicate registrations

Aha na transparency ho hia: beneficiary should know why they’re eligible. Sɛ wopɛ sɛ Ghana’s fintech build trust, “explainability” no yɛ core.

3) Delivery: fa mobile money ne automated payments ma sika du nnipa so

Delivery yɛ baabi a mobile money tumi kɛse wɔ Ghana. Sɛ wode AI ka ho a:

- Auto-scheduling: payments in tranches (e.g., weekly) to reduce sudden agent liquidity pressure

- Dynamic routing: choose the cheapest/most reliable rail (mobile money, bank-to-wallet, voucher rails)

- Fraud controls: flag suspicious patterns (one phone receiving many “households”, repeated cashouts same agent)

Snippet-worthy line: “Sika a ɛboa nkwa no, ɛsɛ sɛ ɛyɛ quick, traceable, na ɛnyɛ easy sɛ obi bɛtwe.”

Drought, war, ne scam networks: asɛm baako pɛ—trust ne identity

RSS no kaa Kenya repatriation from Myanmar scam camps, ne Nigeria ISWAP arrests. Saa nsɛm yi te sɛ “security news,” nanso fintech perspective no mu, wɔn nyinaa ka trust infrastructure ho:

- Scam networks kyerɛ sɛ fraudsters tumi fa digital channels bɔ nnipa.

- Conflict zones kyerɛ sɛ identity documents bɔ wɔn a wɔatu fi fie no.

- Terrorism risks kyerɛ sɛ compliance (AML/CFT) hia, nanso ɛnsɛ sɛ ɛma financial exclusion kɔ soro.

Sɛnea Ghana’s AI fintech bɛma security ne inclusion nyinaa nkɔ anim

Practical approach:

- Tiered KYC: ma nnipa a wɔn nni full documents no ntumi nhyɛ system no mu, nanso wɔn limits yɛ ketewa.

- Device + behavioral signals: fa transaction behavior, device reputation, SIM change patterns ma fraud detection.

- Human-in-the-loop: cases a system flag no, ma agents/field officers verify.

Saa nhyehyɛe yi ma Ghana betumi akɔ so de mobile money rehyɛ akɔntabuo den, bere a ɔman no resi so yɛ tourism branding ne diaspora engagement wɔ December mu.

Ghana context: “December economy” kyerɛ adwuma a yɛbɛtumi ayɛ

AllAfrica content no kae sɛ Ghana anya visitors bɛboro 125,000 last December, na government pɛ sɛ ɛkwati “Detty December” label. M’ani gye ho sɛ branding debate no wɔ hɔ—nanso asɛm a ɛsom bo kɛse ne sɛ: December economy no kyerɛ sɛ Ghana tumi gye transactions volume kɛse, cross-border remittances, ne merchant payments.

Sɛ yɛtumi yɛ saa bere yi mu payments yi yie a:

- merchants nya working capital data

- banks/fintechs tumi offer micro-loans a ɛyɛ responsible

- government tumi hu tax base/levies more accurately (sɛ policy no yɛ balanced)

- diaspora tumi tua fees, rent, school, ne donations without friction

Na sɛ crisis ba a (floods, price shocks), saa rails yi na yebetumi de emergency disbursements ayɛ.

Example blueprint: “Emergency Wallet” for Ghana (practical)

Sɛ institution bi (municipal assembly, NGO, corporate CSR) pɛ sɛ ɔboa mpɔtam bi a nsuo ayɛ wɔn dɛn a:

- Register households (basic KYC)

- Create wallets / link existing mobile money accounts

- Use AI to prevent duplicates and prioritize most vulnerable

- Disburse in small tranches

- Provide spending controls (optional): e.g., part as unrestricted cash, part as voucher for essentials

- Audit dashboard: who received, when, where, anomalies

This matters because: funding might be limited, but misallocation shouldn’t be tolerated.

“People also ask” (FAQ) — AI fintech ne crisis payments

AI bɛtumi asi corruption ano wɔ cash aid mu anaa?

Aane—sɛ wode end-to-end traceability (wallet logs), anomaly detection, ne independent audit dashboards bɔ mu. Nanso ɛsɛ sɛ governance wɔ hɔ: who can approve payments, what thresholds, and periodic reviews.

Mobile money nko ara ntumi mma mmoa adu nnipa so anaa?

Ɛtumi boa kɛse, nanso problem bi te sɛ duplicate registrations, SIM swap fraud, agent liquidity, ne wrong targeting no betumi ama impact tew. AI ne automation na ɛma “delivery” no yɛ reliable.

Sɛ network down a, ɛbɛyɛ dɛn?

Crisis design must assume downtime:

- multi-rail payouts (two telcos or telco + bank)

- offline voucher fallback for extreme cases

- staged payments so backlog doesn’t explode

Nea businesses, NGOs, ne fintech founders bɛyɛ afei (action list)

Sɛ woreyɛ fintech anaa wode mobile money di dwuma wɔ Ghana a, fa saa checklist yi yɛ adwuma wɔ 2026 planning mu:

- Build a payout engine: bulk disbursements + reconciliation + beneficiary management.

- Add AI fraud detection: SIM swap alerts, unusual cashout loops, agent risk scoring.

- Design explainable eligibility: beneficiaries should understand decisions.

- Plan liquidity with agents: forecast volumes, pre-fund hotspots, stagger payouts.

- Measure outcomes: attendance return (school), food basket stability, time-to-receive funds.

Stance: Sɛ fintech wɔ Ghana pɛ sɛ ɛyɛ “real economy” tool a, ɛnsɛ sɛ ɛgyina merchant payments nkutoo so. Crisis payouts ne social protection rails no yɛ baabi a credibility fi.

Nea ɛdi akyi: AI-led fintech sɛ resilience infrastructure

Somalia drought no ne Sudan ko no yɛ nhoma a ɛkyerɛ yɛn sɛ sika a ɛba mmoa mu no betumi asɔre anaa asiane, nanso delivery efficiency yɛ ade a yebetumi asiesie. Ghana wɔ advantage: mobile money adoption, fintech talent, ne diaspora flows.

Sɛ “AI ne Fintech: Sɛnea Akɔntabuo ne Mobile Money Rehyɛ Ghana den” series no botaeɛ yɛ sɛ yɛma adwuma ayɛ mmerɛw, yɛma ahotosoɔ sɔre, na yɛma automation boa wɔn a wɔyɛ adwuma ne wɔn a wɔgye sika. Saa post yi de asɛm no kɔ akyirikyiri: mobile money + AI = sika a ɛteɛ, a wotumi di akyi, na wotumi de si nkwa so.

Sɛ wo yɛ NGO, fintech founder, anaa business a wo pɛ sɛ wode automated payments anaa AI fraud detection ma wo mobile money operations mu yɛ den a, hyɛ aseɛ na yɛnhyehyɛ pilot bi wɔ 2026 Q1–Q2. Crisis no ntwe yɛn akyi—nanso yebetumi asiesie rails a ɛma yɛtumi gyina mu.

Dɛn na wobɛpɛ sɛ wosɔ hwɛ kan: bulk payouts, fraud detection, anaa beneficiary targeting?