Visa’s Johannesburg data centre strengthens local payments—speed, resilience, compliance—and sets up SA e-commerce teams to scale AI fraud, checkout and support.

Visa’s SA Data Centre: The AI Boost for Payments

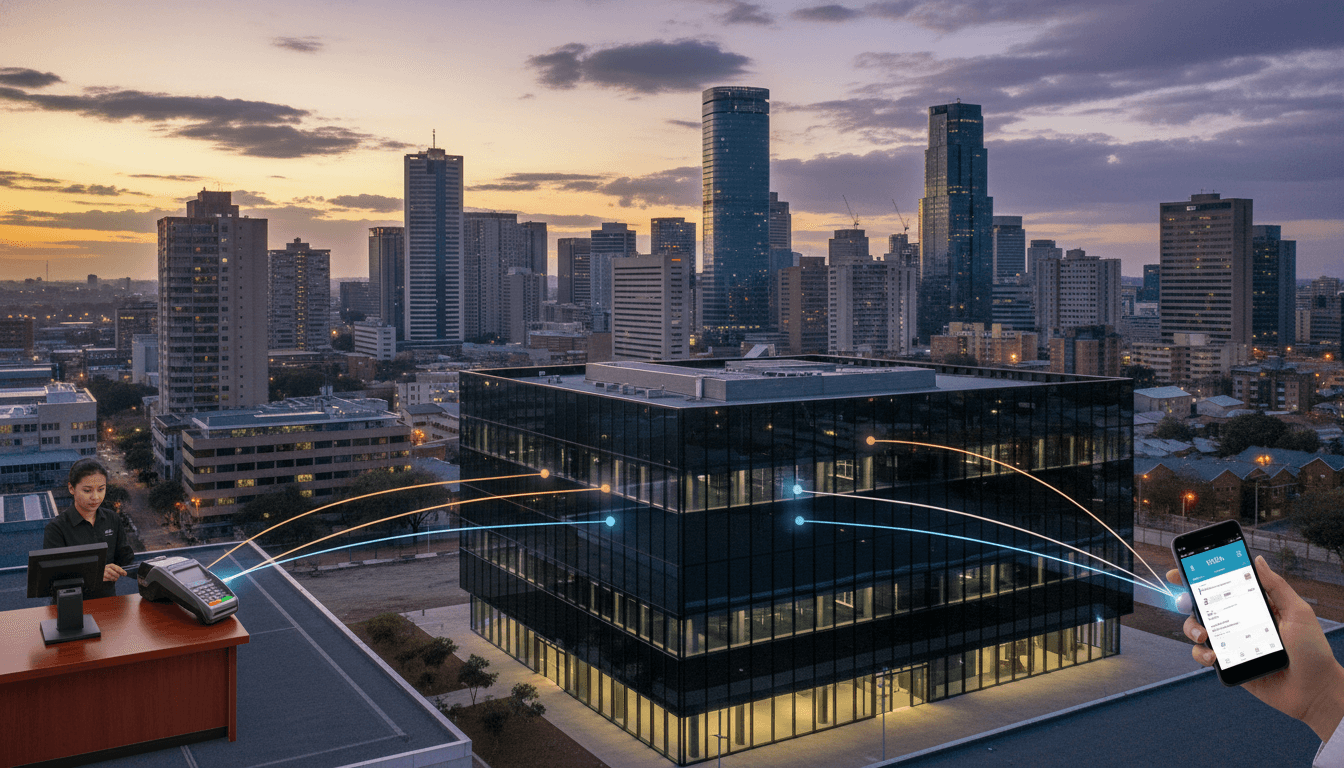

R1 billion over three years is a loud signal in any market. Visa’s decision to put that money behind a Johannesburg data centre (launched in July 2025, and Visa’s first on the African continent) isn’t just a payments story—it’s a digital infrastructure story. And infrastructure is what decides whether AI in e-commerce and digital services stays stuck in pilot mode or becomes everyday reality.

If you sell online in South Africa—or you’re building a fintech product that touches payments—your AI ambitions live or die on a few unglamorous basics: latency, uptime, compliance, and access to rich, reliable transaction signals. Visa’s local VisaNet node changes the baseline for all of that. It brings transaction authorisation, routing, and settlement closer to where customers tap, click, and pay.

Why a local Visa data centre matters for AI in e-commerce

A local Visa data centre matters because AI systems perform better when the underlying payment network is fast, predictable, and compliant. AI can personalise, detect fraud, optimise conversions, and automate support—but those benefits get muted if checkouts time out, tokenisation calls lag, or “false declines” spike during peak shopping periods.

Visa’s Johannesburg facility processes domestic transactions for multiple financial institutions, including banks, acquirers, and fast-growing fintechs. Visa’s SA leadership has described broad migration of local Visa partners to the centre for domestic processing. The practical outcome: less distance for transactions to travel, fewer hops, fewer points of failure.

The AI connection: better data in, better decisions out

Most e-commerce AI use cases rely on event streams: payment attempts, authorisations, reversals, refunds, chargebacks, device signals, and behavioural patterns around checkout. When transaction processing is local and stable, the data becomes:

- More timely (useful for real-time decisions)

- More consistent (fewer gaps from intermittent network issues)

- More governable (easier to manage data handling rules)

That’s the difference between an AI model that reacts now and one that only explains what happened yesterday.

Speed, reliability, and fewer failed checkouts (the part customers feel)

Here’s the blunt truth: checkout failures are a revenue leak disguised as “tech issues.” Every extra second at payment increases drop-off. And when a transaction times out, you don’t just lose the sale—you often lose the customer’s confidence.

By processing domestic transactions closer to their origin, a local VisaNet node can reduce latency and help prevent avoidable timeouts. For merchants, that shows up as more consistent point-of-sale performance for:

- High-volume card payments

- Contactless tap-to-pay

- Mobile wallet transactions

- Peak seasonal spikes (December is the obvious stress test)

Where AI compounds the benefit

Faster, more reliable payments create room for AI to work properly at the moment that matters most: conversion.

Examples South African online retailers are actively prioritising right now:

- AI checkout optimisation: models that detect friction (failed attempts, repeated CVV retries, switching payment methods) and trigger immediate interventions.

- Dynamic authentication orchestration: routing customers into step-up verification only when risk is high, reducing unnecessary friction.

- Agent-assist customer support: when a payment fails, AI can pull the right payment status quickly and generate a clear explanation to the customer.

A local payments backbone doesn’t replace these systems—it makes them worth building.

Data sovereignty and compliance: the “boring” advantage that unlocks product

Local infrastructure has a second-order effect that product teams often underestimate: it makes compliance less of a blocker.

South African regulators (like their counterparts globally) are increasingly focused on data residency and cross-border data flows—especially for sensitive financial data. Visa’s domestic processing capability can help banks and fintechs keep certain transaction data within South Africa, simplifying operational complexity that comes with routing payments through offshore facilities.

Why this matters for AI-driven digital services

AI projects frequently stall when teams can’t answer basic questions:

- Where is the data processed?

- Who can access it?

- How is it retained and audited?

When more processing occurs locally, it’s easier to build a compliance story that stands up to procurement reviews, partner due diligence, and regulator expectations.

Good AI governance starts with good infrastructure. If your data flows are messy, your model risk management will be messy too.

Resilience and redundancy: the quiet upgrade that reduces systemic risk

Visa has positioned the Johannesburg data centre as part of improving resilience across the payments ecosystem—local processing with built-in redundancy reduces dependence on international network routes and can mitigate the blast radius of global outages.

For merchants and platforms, that translates into fewer “we can’t take card payments right now” moments. And that matters more in 2025 than it did a few years ago, because:

- Customers expect digital payments everywhere

- On-demand delivery and subscription services can’t pause easily

- E-commerce peaks are sharper (promotions, payday spikes, holiday surges)

AI and resilience: fraud doesn’t wait for business hours

Fraud attempts surge during high-traffic periods—exactly when networks are under strain. AI fraud detection thrives when:

- transaction scoring happens consistently,

- the pipeline doesn’t drop events,

- and you can respond in milliseconds.

Local processing helps stabilise those conditions. That doesn’t mean fraud disappears. It means your detection and response tools get a fair fight.

Why Visa’s facility isn’t “just another cloud region”

One detail from Visa’s SA leadership is worth taking seriously: a payments data centre isn’t the same thing as a general-purpose public cloud.

Cloud platforms are designed for broad workloads and elastic scaling. Visa’s payments facility is described as purpose-built for deterministic transaction routing, ultra-high availability, and payment-industry compliance standards like PCI-DSS.

What “purpose-built for payments” means in practice

For e-commerce and fintech teams, it usually means:

- Predictable transaction behaviour (less jitter, fewer surprise bottlenecks)

- Stronger compliance posture for payment data handling

- Better support for payment-specific services such as tokenisation, card vaulting, and fraud analytics

Those services are key building blocks for AI-powered commerce.

Tokenisation, for example, supports safer digital checkout experiences (and can reduce fraud exposure). Card vaulting enables subscription billing and one-click payments. Fraud analytics feeds the risk engines that decide whether to approve, step up, or block.

What this enables for South African fintechs and online retailers

The Johannesburg data centre gives fintechs faster and more predictable access to Visa services. That “predictability” is underrated: it shortens build cycles.

Here are practical ways South African businesses can use the improved foundation to ship AI-powered capabilities faster.

1) AI-driven fraud prevention tuned for SA patterns

Off-the-shelf fraud models trained on global patterns often misread local context—device sharing, payment behaviour differences across provinces, and merchant category nuances.

A better approach:

- Start with vendor/partner fraud analytics signals

- Add your own first-party signals (account age, delivery address confidence, refund behaviour)

- Retrain on your own outcomes (chargebacks, confirmed fraud, friendly fraud)

This is where stable payment telemetry helps. You can’t train models on missing or inconsistent event data.

2) Smarter declines management (and fewer false declines)

False declines are expensive: you lose revenue and annoy good customers. Infrastructure improvements that reduce timeouts are step one. Step two is AI.

Tactics that work:

- Real-time retry logic based on decline reason and customer history

- Payment method recommendations (instant EFT vs card vs wallet) personalised to the shopper

- Risk-based step-up (only add friction when it’s justified)

3) AI personalisation that respects privacy and compliance

South African consumers are price-sensitive and value convenience. AI can increase conversion with better product recommendations, bundling, and targeted offers. But personalisation also raises governance issues.

A practical middle ground I’ve found works well:

- Personalise using first-party behavioural data and transaction outcomes you’re allowed to use

- Keep your models transparent enough to explain decisions to business stakeholders

- Bake retention rules and access controls into your data pipeline early

Local processing infrastructure helps because it reduces complexity in data flows and policy enforcement.

4) Faster experimentation for digital services

If you run a digital service—subscription content, mobility, insurance, or on-demand delivery—payments are your heartbeat. When authorisation is reliable, you can safely run A/B tests on:

- pricing and packaging

- trial-to-paid journeys

- saved card vs wallet prompts

- renewal retry schedules

AI thrives in environments with frequent, measurable feedback loops. Payments provide that feedback.

A South African reality check: infrastructure first, AI second

Most companies get this wrong. They start with AI tooling, hire a consultant, build dashboards, and then discover that their checkout is brittle, their payment data is fragmented, and their compliance story is shaky.

Visa’s Johannesburg data centre is a reminder that AI progress is often won in the plumbing:

- local processing that reduces latency

- resilience that reduces downtime

- compliance alignment that reduces procurement friction

- payment-grade services (tokenisation, vaulting, fraud analytics) that reduce build effort

Visa also noted job creation and skills development linked to the investment, including specialised roles across data engineering, payments infrastructure, analytics, and business development. That matters because talent concentration tends to attract more product building—especially in fintech.

What to do next if you’re building AI-powered commerce in SA

If you’re an online retailer, fintech, or digital service provider, treat this moment as an invitation to tighten your stack.

Start with a short audit:

- Measure payment latency and timeout rates during peak traffic (not average days).

- Map your payment data flow end-to-end: what you store, where it moves, and who touches it.

- Identify the top two revenue leaks at checkout (false declines, failed 3DS, customer confusion, refund friction).

- Pick one AI use case tied directly to money: fraud reduction, decline recovery, or support automation.

If your foundation is solid, AI becomes a practical tool—not a science project.

The bigger question for 2026 is simple: as South Africa’s payments infrastructure becomes more local and resilient, which businesses will use that stability to build smarter customer experiences—and which will keep blaming “payment issues” for lost sales?