Sodium-ion batteries just landed a 4.75GWh deal in the US. Here’s why that matters for grid-scale storage, safety, and the next wave of green technology projects.

Most companies planning large-scale energy storage in 2026–2030 are all chasing the same thing: lithium-ion capacity that’s getting more expensive, more constrained, and harder to permit. That’s exactly why the latest deal between Peak Energy and Jupiter Power matters.

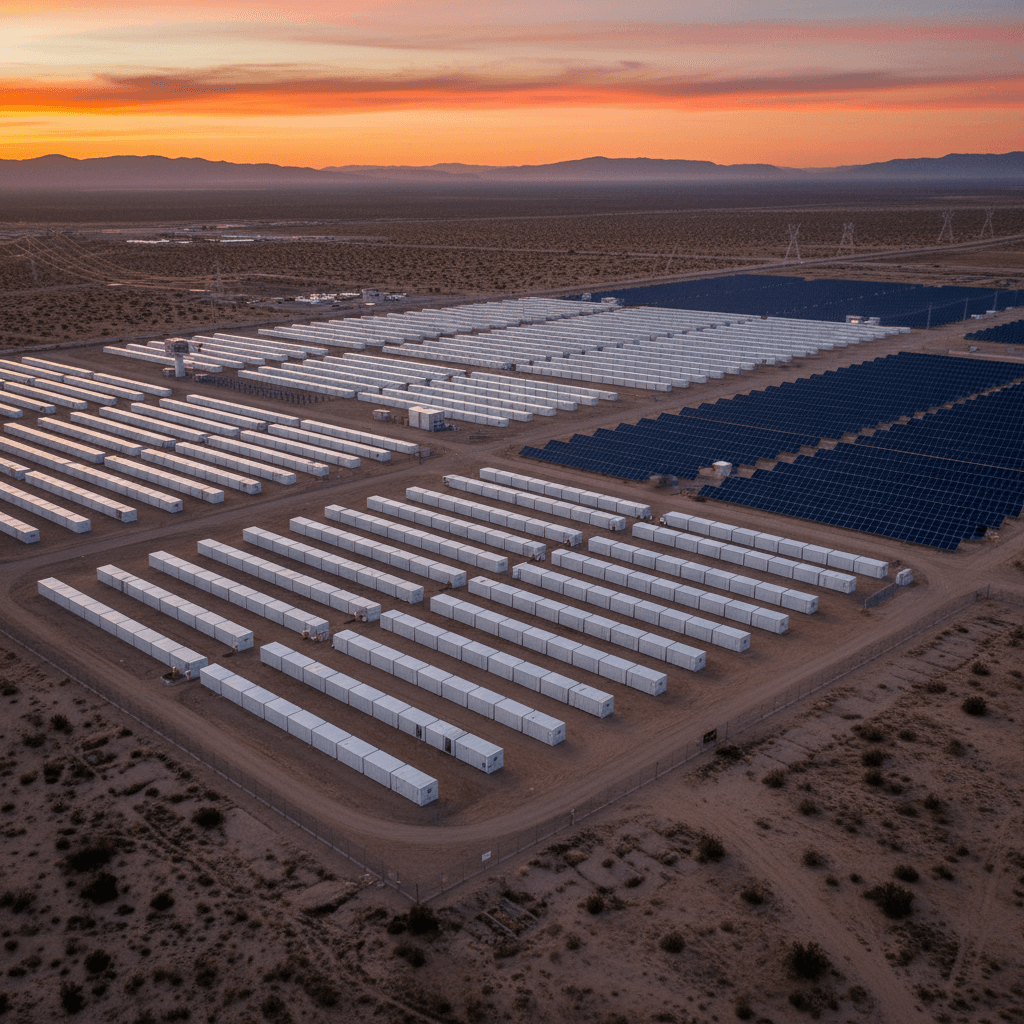

Peak Energy, a US sodium‑ion battery startup, has just locked in a multi‑year agreement to supply up to 4.75GWh of sodium‑ion battery energy storage systems (BESS) to Jupiter Power, including a firm 720MWh project for 2027. The contract value could pass US$500 million. For a technology many people still think of as “emerging,” that’s a serious commercial vote of confidence.

This isn’t just another storage contract announcement. It’s a signal that non‑lithium energy storage is moving from pilot projects to bankable infrastructure—and it sits right at the intersection of green technology, national security, and smarter grid design.

In this post, I’ll break down what’s actually happening in this deal, why sodium‑ion is getting traction now, and what it means if you’re building, financing, or operating clean energy assets in the US over the next decade.

Sodium-Ion BESS: What’s Really Changing Here

The key shift is this: sodium‑ion batteries are now being ordered at multi‑GWh scale for grid storage, not just tested in labs or single‑container pilots.

Peak Energy will supply Jupiter Power with sodium‑ion BESS using its sodium‑ion phosphate pyrophosphate (NFPP) chemistry for deployments between 2027 and 2030. One 720MWh project is a firm order; the remaining ~4GWh is under capacity reservation. For developers, that’s exactly how you de‑risk a new chemistry: start with a committed anchor project, then stage in larger capacity as performance data comes in.

From a green technology perspective, this is a big deal for three reasons:

- Chemistry diversification – Getting off a single‑chemistry dependence (lithium‑ion) makes the clean energy transition more resilient.

- Domestic supply chain – Peak is explicitly focused on onshoring battery manufacturing in the US, supported by federal policy like H.R.1.

- Safety and siting flexibility – Sodium‑ion is being positioned as a safer alternative for high‑capacity installations near sensitive assets.

The reality? Sodium‑ion isn’t trying to beat lithium at everything. It’s targeting the segments where energy density is less important than cost, safety, and supply security—exactly the sweet spot for stationary grid storage.

Why Sodium-Ion Fits Grid-Scale Storage (Better Than Many Think)

For grid storage, energy density is useful but not king. Land is usually cheaper than rare metals, and what really drives value is cost per kWh, lifetime, safety profile, and how fast you can deploy.

Here’s how sodium‑ion slots into that picture.

1. Abundant, Less Geopolitically Exposed Materials

Lithium, nickel, and cobalt supply chains are geographically concentrated and politically sensitive. Sodium, by contrast, is abundant almost everywhere.

That has several practical advantages for green technology projects:

- More predictable pricing than lithium-based chemistries

- Lower exposure to single‑country supply disruptions

- Easier alignment with national industrial policy around “friend‑shored” or domestic production

Peak Energy’s leadership has been blunt about this: from a national security perspective, the ability to store energy domestically using locally manufactured materials is non‑negotiable long term.

2. Safety That Changes Where You Can Build

High‑energy lithium‑ion systems bring real fire and thermal runaway risk. They’re getting safer, but you still see developers and communities worrying about 100MWh+ installations near industrial plants or data centers.

As Mukesh Chatter, CEO and co‑founder of another sodium‑ion player, Alsym Energy, has argued:

“If you go to high‑density applications, 200kWh, 1MWh, multi‑MWh, it’s just too dangerous.”

His point isn’t that lithium is unusable. It’s that risk tolerance changes once you’re stacking tens or hundreds of megawatt‑hours.

Sodium‑ion cells generally operate with less flammable materials and lower runaway energy. For developers, that can translate into:

- Fewer siting conflicts with local communities

- Better fit next to chemical plants, metal processing, and data centers

- Potentially leaner fire suppression and safety systems (subject to code and AHJ approval)

It’s not magic, but it’s a meaningful shift—especially as grid operators, RTOs, and hyperscale data center owners start specifying stricter safety criteria in RFPs.

3. Performance That’s Good Enough for the Use Case

Sodium‑ion batteries typically offer:

- Lower energy density than lithium‑ion (you need more space per kWh)

- Competitive cycle life for stationary storage

- Strong performance in cold or variable environments for certain chemistries

For utility‑scale BESS installed on cheap land or integrated with solar farms, the trade‑off is often acceptable:

- You’re not space constrained like an EV

- You are highly sensitive to cost, supply security, and safety

That’s why you’re seeing sodium‑ion appear first in grid‑scale projects, microgrids, and behind‑the‑meter commercial storage, not in passenger vehicles.

Inside Peak Energy’s Sodium-Ion Strategy

Peak Energy isn’t just selling a new battery chemistry; it’s trying to build a vertically aligned, US‑based sodium‑ion platform that fits modern grid needs.

NFPP Chemistry and System Design

Peak’s systems use sodium‑ion phosphate pyrophosphate (NFPP) cells. On top of the chemistry, the company is designing:

- BESS without moving parts in the core stack

- Integrated active cooling and ventilation

The claim is that this architecture removes many common failure points from traditional BESS systems. Fewer mechanical components and well‑managed thermal conditions mean:

- Less system degradation over time

- Reduced need for mid‑life augmentation (adding extra batteries to maintain capacity)

- More predictable long‑term performance for project financiers

From a project finance perspective, that matters. Storage projects pencil out much better when you can:

- Avoid unplanned capex in year 7–10

- Model a flatter degradation curve in your pro forma

- Bid confidently into long‑term capacity, ancillary services, and tolling agreements

From Pilot to Commercial Scale

Peak has followed a fairly classic green technology commercialization path:

- Pilot at SolarTAC (Watkins, Colorado) – Deployed sodium‑ion BESS in partnership with nine utilities and IPPs, focused on gathering operational and modeling data.

- Engineering center in Broomfield, CO – Announced near the end of 2024, working with the Colorado Office of Economic Development and International Trade (OEDIT).

- US cell factory – Under development, with production targeted for 2026, giving the Jupiter Power projects a domestic supply base.

What I like about this approach is that it lines up technology readiness, manufacturing capacity, and commercial demand along the same timeline:

- 2024–2025: Prove performance with utilities and IPPs

- 2026: Start producing cells at scale

- 2027–2030: Deliver multi‑GWh BESS orders like the Jupiter portfolio

For corporate buyers and utilities watching green technology trends, this is a sign sodium‑ion is maturing into something you can actually plan around—not just buzzword material for slide decks.

What This Means for Developers, Utilities, and Investors

If you’re working on clean energy, grid planning, or infrastructure investment, the Peak–Jupiter deal offers a few practical signals.

1. Start Treating Sodium-Ion as a Real Option in RFPs

From 2027 onward, sodium‑ion BESS will be a credible response to large‑scale storage RFPs—especially where safety and domestic content are high priorities.

Where it could fit well:

- 4‑hour or longer duration projects in heat‑stressed or fire‑sensitive regions

- Storage collocated with industrial facilities and data centers

- Markets or programs that reward domestic content or low‑carbon manufacturing

You don’t need to replace all your lithium‑ion assumptions overnight. But it’s smart to begin modeling sodium‑ion as a parallel case in your procurement scenarios, especially for projects that will COD in 2027–2030.

2. Revisit Your Risk Model Around Safety and Community Acceptance

Community pushback is quickly becoming one of the hidden costs of big BESS projects. A technology with a safer materials profile and lower runaway energy doesn’t erase risk, but it does:

- Strengthen your hand in public consultations

- Help with permitting near sensitive loads and critical infrastructure

- Reduce reputational risk in the event of an incident

If you’re running ESG‑filtered capital, sodium‑ion and other non‑lithium technologies can also improve the story you tell limited partners about long‑term sustainability and resilience.

3. Align Storage Strategy With Domestic Manufacturing Policy

US federal policy is steadily rewarding onshore clean energy manufacturing. Peak Energy has designed its business to fit right into that environment:

- US‑based engineering and production

- Chemistries that use more abundant, less politically sensitive materials

If you’re a developer or IPP targeting US markets, it’s worth asking:

- How much of my 2027–2035 pipeline is exposed to imported battery supply chains?

- Where could sodium‑ion or other non‑lithium techs reduce exposure and improve policy alignment?

The trend across the green technology space is clear: projects that align with industrial policy get built faster and financed easier.

How AI and Data Will Help Sodium-Ion Compete

This blog series focuses on green technology and AI for a reason: the next wave of clean energy growth won’t just be about new hardware; it’ll be about smarter, data‑driven operation.

Sodium‑ion storage is a great example. To compete with lithium‑ion, it needs to prove itself on:

- Real‑world cycle life

- Degradation patterns under different duty cycles

- Response under extreme weather and grid events

That’s where AI and advanced analytics come in:

- Utilities and developers can use machine learning models to compare lithium‑ion and sodium‑ion performance across thousands of operating hours.

- Asset operators can optimize dispatch strategies specifically tuned to sodium‑ion characteristics, rather than copying lithium playbooks.

- Manufacturers like Peak can feed operational data back into cell design, thermal management, and control algorithms, tightening the loop between R&D and field performance.

Over time, the projects that win won’t just be the ones with cheaper chemistry. They’ll be the ones that use AI‑driven control and forecasting to squeeze maximum value out of each installed kWh while extending asset life.

Where This Fits in the Bigger Green Technology Story

Sodium‑ion doesn’t replace lithium‑ion, pumped hydro, or flow batteries. It adds another tool to the green technology toolbox at a time when demand for energy storage is exploding—from PJM’s multi‑GW interconnection queues to Germany’s 24GW storage forecast by 2037.

Here’s the thing about transitions: they succeed when there are multiple viable paths, not one fragile, over‑optimized supply chain. Peak Energy’s 4.75GWh agreement with Jupiter Power is one more proof point that we’re heading toward a more plural, more resilient storage ecosystem.

If you’re planning infrastructure in the late 2020s, it’s no longer enough to know “storage = lithium‑ion.” You’ll need a working understanding of sodium‑ion, flow, and other non‑lithium technologies—and a strategy for where each fits.

My advice: start that work now, while projects like Peak’s SolarTAC deployment and upcoming Jupiter portfolio are still early enough that you can learn from them, not just compete with them.

The next few years will decide which technologies become standard in grid‑scale storage. Sodium‑ion has just taken a big step out of the pilot phase. The question is whether your planning, procurement, and modeling assumptions are keeping up.