Germany’s latest 213MWh of battery storage from Statkraft, Kyon and Juniz shows how solar-plus-storage, smart financing and AI optimisation are reshaping green energy.

Most investors underestimate how quickly battery storage is turning into critical energy infrastructure in Europe. Germany is the clearest proof right now.

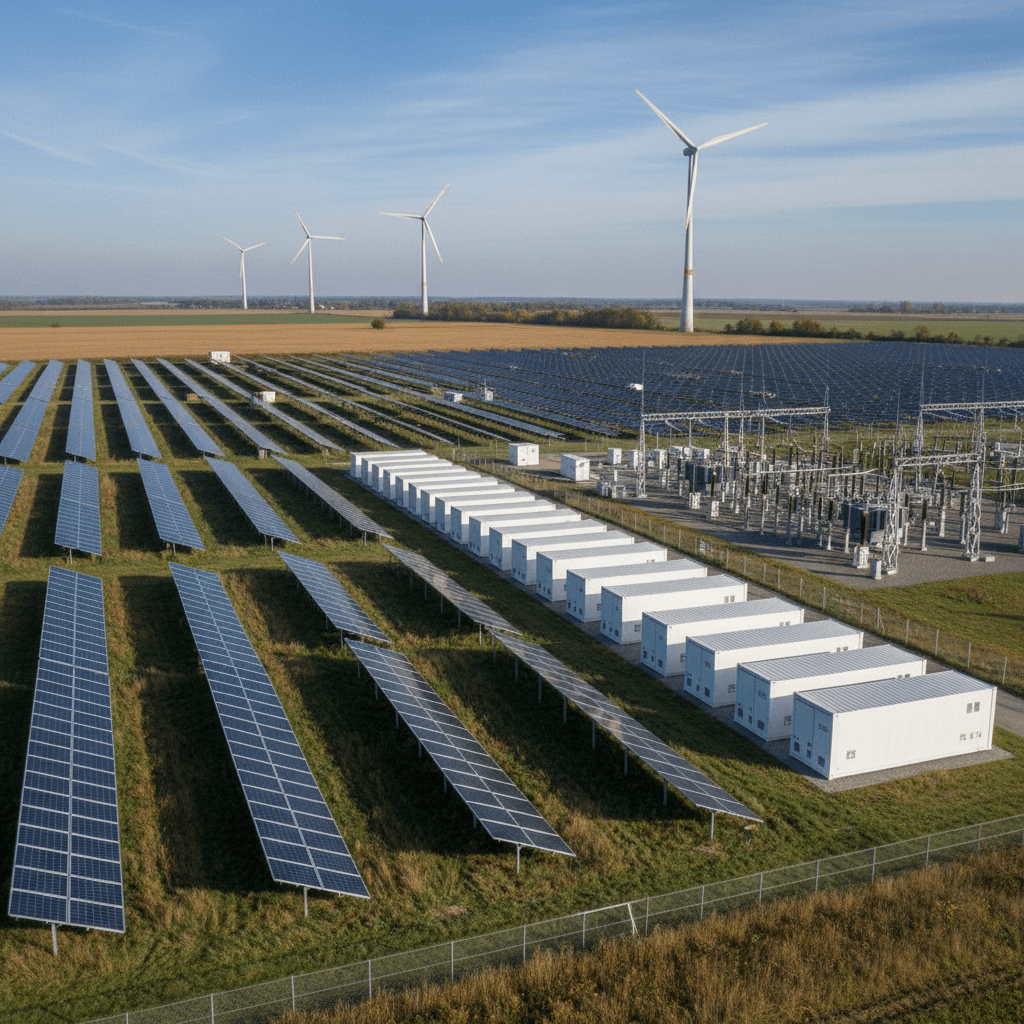

Over just a few weeks, three players — Statkraft, Kyon Energy and Juniz Energy — moved forward with 213MWh of new battery energy storage systems (BESS) in Germany. That’s on top of multiple 700MWh projects and a 1GW/4GWh giant already in the pipeline. This isn’t a side story anymore; it’s the backbone of a low‑carbon power system forming in real time.

This matters because storage is what turns green technology from “nice” to “reliable.” Solar and wind give you cheap clean energy. Batteries make it dispatchable, tradable and bankable.

In this article, I’ll break down what Statkraft, Kyon and Juniz are actually doing, why Germany has suddenly become Europe’s storage hotspot, and what this means if you’re a developer, investor, utility or large energy user looking at clean energy and AI‑driven optimisation as a growth opportunity.

Germany’s BESS boom: why 213MWh is more than just a number

Germany is now the most attractive battery storage market in Europe because the fundamentals line up: deep power markets, volatile prices, clear regulation, and a massive build‑out of renewables.

The 213MWh of new activity from Statkraft, Kyon and Juniz sits on top of:

- Multiple c.700MWh projects starting construction

- A 1GW/4GWh storage project targeting 2027/28

- Continuous upgrades to market rules that finally treat storage as its own asset class

For green technology as a whole, Germany is a live demo of what a storage‑centric grid looks like:

- Solar-plus-storage hybrids compete directly with fossil plants

- Batteries trade across multiple markets in the same day

- AI‑driven trading software squeezes extra value out of every MWh

The reality? If you want to understand where profitable green infrastructure is heading in 2026–2030, Germany is the case study to watch.

Statkraft’s solar-plus-storage plant: the hybrid model in action

Statkraft has just commissioned Germany’s largest solar-plus-storage project under the Renewable Energy Sources Act (EEG) “innovation tender” framework — a signal of where policy and capital are both headed.

- Solar capacity: 46.4MW

- Battery capacity: 16MW / 57MWh

- Investment: €45 million

- Technology: 88 “battery cubes”, almost certainly Fluence hardware

- Status: Feeding power into the grid since October 2025, final grid tests underway

How the ‘innovation tender’ changes the game

The innovation tender under the EEG doesn’t just subsidise solar or wind; it rewards hybrid plants that integrate storage and charge it from renewables. That’s a quiet but important shift.

Here’s why this framework works:

- It favours firm, controllable green power instead of just raw capacity

- Developers are nudged to design smart, AI‑optimised systems, not just PV fields

- Revenue isn’t only about feed‑in tariffs; it’s about capturing spreads between times of high and low prices

From a green technology perspective, Statkraft’s project is textbook:

- Daytime: Solar over‑production charges the battery instead of being curtailed.

- Evening peaks: The battery discharges when wholesale prices and grid stress are highest.

- AI optimisation: Algorithms can decide whether a given MWh is more valuable in the day‑ahead market, intraday, balancing markets or ancillary services.

You end up with an asset that isn’t just “green” — it’s profitable infrastructure that competes with gas peakers and stabilises the grid.

Why this matters for developers and utilities

If you’re planning new renewable capacity in Europe, the message is blunt: standalone solar is already behind the curve in markets like Germany. Hybridising with BESS is fast becoming the default because:

- Banks increasingly prefer projects with diversified revenue streams

- Grid operators like assets that help system stability rather than creating congestion

- Policy frameworks are slowly aligning to support storage‑backed renewables

I’ve seen this pattern across markets: once a country proves a bankable hybrid model at scale, copy‑paste adoption comes very quickly.

Kyon Energy and Canadian Solar: storage as a flexible, multi‑vendor ecosystem

Kyon Energy, a German BESS platform owned by TotalEnergies, has lined up 20.7MW / 56MWh of storage for a project in Lower Saxony. The storage will be supplied by Canadian Solar’s e‑Storage business, using its Solbank solution, with shipments kicking off in March 2026.

Two points stand out here.

1. Long-term service is becoming the norm

The deal includes a 20‑year long-term service agreement (LTSA). That’s not window dressing; it’s a core part of the business case:

- Batteries degrade, software changes, grid rules evolve

- Bankers don’t want to underwrite “mystery performance” past year 7

- A robust LTSA gives confidence on availability, efficiency and response time over the asset’s life

If you’re structuring a project right now, you almost never want to treat the battery as pure capex. You want long‑horizon O&M baked in, ideally backed by strong warranties and performance guarantees.

2. Multi-supplier strategies are becoming strategic

TotalEnergies already owns Saft, its in‑house BESS integrator, which is delivering 321MW of storage for seven Kyon projects. Yet for this Lower Saxony site, Kyon is going with Canadian Solar e‑Storage instead.

That’s a deliberate move — and frankly, a smart one:

- It avoids technology lock‑in and pricing dependence on a single vendor

- It lets Kyon match specific projects with the most suitable tech stack (thermal design, container configuration, software, warranty, etc.)

- It keeps suppliers competing, which tends to show up as better commercial terms and better support

For the broader green technology ecosystem, this is exactly what you want to see: a modular, multi‑vendor landscape where developers can pick the right combination of hardware, software, AI and financing.

If you’re building a portfolio, I’d seriously consider:

- At least two storage vendors across your pipeline

- Standardised data interfaces and control systems, so assets can plug into a unified AI optimisation layer even if the containers come from different manufacturers

Juniz Energy and HCOB: why financing is now the real bottleneck

Juniz Energy (styled ju:niz), another Germany‑focused BESS platform backed by EQT, has just secured financing from Hamburg Commercial Bank (HCOB) for three battery projects totalling around 100MWh.

HCOB stepped in as lender, agent, account bank and hedging bank. That combination tells you two things:

- BESS is now a mainstream asset class in project finance

- The real value is in structuring and risk management, not just hardware

What banks are really looking for in BESS projects

From conversations I’ve had around the sector, most lenders now want to see:

- Multiple revenue streams: spot arbitrage, balancing markets, capacity mechanisms where available

- Route‑to‑market clarity: who trades the asset, with what algorithms, under what contracts

- Solid counterparties: reputable EPCs, proven integrators, bankable LTSA providers

- Regulatory fit: clear grid connection, compliance with storage rules, no hidden curtailment risks

Juniz’s CFO put it plainly: flexible, attractive financing is a core value driver, not an afterthought. In other words, the winners in green technology won’t just be the ones with good hardware — they’ll be the ones with capital stacks that match the operational reality of storage.

Actionable lessons for storage developers and investors

If you’re trying to bring a BESS pipeline from pitch deck to NTP, this German example gives a useful checklist:

- Standardise your project docs across the portfolio so banks can underwrite a “template” rather than one‑offs

- Get your trading strategy and optimiser (often AI‑based) agreed early; don’t bolt it on after financing

- Structure contracts so that performance risk and merchant risk are clear — and ideally partly hedged

- Build long‑term relationships with a small group of banks that understand storage rather than constantly shopping deals

In 2026–2028, the constraint on storage build‑out is more likely to be bankable business models and grid capacity than cell supply.

How AI and software turn BESS into high-value green assets

All three of these German projects sit inside a broader shift: batteries are becoming software‑defined, AI‑optimised revenue machines rather than just big boxes of cells.

A modern grid‑scale battery in Germany can:

- Charge from cheap midday solar

- Discharge into evening peak wholesale prices

- Provide primary and secondary reserves within seconds

- Support local voltage or congestion constraints

- Shift behaviour daily based on updated AI forecasts

That’s several markets, several risk profiles, and often machine‑learning models deciding in real time where each MWh goes.

For companies building or using green technology, here’s where AI is already making a difference:

- Forecasting: Better price and imbalance forecasts turn every project into a more bankable asset

- Real‑time optimisation: Algorithms manage cycle depth, state‑of‑charge and degradation to extend life and maximise revenue

- Portfolio coordination: Multiple BESS assets, solar farms and even flexible loads can be orchestrated together like a virtual power plant

If you’re a large energy user, data centre operator, or industrial group, this same stack can be applied behind the meter:

- Use on‑site solar + BESS to avoid peak grid charges

- Time‑shift consumption to low‑carbon hours, tracked via granular carbon accounting

- Monetise flexibility by participating in ancillary markets via an aggregator

The hardware makes it green. The software and AI make it profitable and scalable.

Where this fits in the Green Technology story — and what to do next

Germany’s 213MWh of new BESS progress from Statkraft, Kyon and Juniz isn’t an isolated headline. It’s part of a pattern we’re seeing across this Green Technology series: clean energy becomes truly dominant not just when we build more megawatts, but when we add intelligence, flexibility and finance that actually work together.

If you’re in the energy, sustainability or infrastructure space, the direction of travel is clear:

- Expect more hybrid solar‑plus‑storage projects instead of standalone PV

- Expect AI‑driven optimisation to move from optional to essential

- Expect lenders and equity investors to ask tougher, smarter questions about revenue stacking and long‑term performance

The better way to approach this is to treat storage as a central planning assumption, not a future add‑on. Whether you’re:

- A developer building your next project pipeline

- A corporate buyer setting a 24/7 clean energy strategy

- An investor looking for resilient, inflation‑linked cashflows

…you should be actively asking: What is my storage strategy, and how does AI‑driven optimisation fit into it?

Because the markets that figure this out — like Germany is doing right now — won’t just hit their climate targets. They’ll own the next decade of energy economics.