Italy’s MACSE tariffs look low, but smart, AI-driven BESS asset management can turn 15-year contracts into strong, resilient returns in a renewables-heavy grid.

Why Italy’s Battery Revenues Are Low Now – And Why That’s OK

Italian battery storage projects just locked in 15-year contracts at some of the lowest MACSE tariffs anyone expected. A lot of developers looked at those numbers and quietly wondered: did we just price the risk wrong?

Here’s the thing about Italy’s MACSE and capacity market revenues: they look thin today, but they’re likely to become more valuable over time as the power system decarbonises. For investors, grid operators and green technology players, the opportunity isn’t gone – it’s just shifting from easy margins to smart operations and AI-enabled asset management.

This article breaks down what’s happening in Italy, why low tariffs aren’t necessarily bad news, and how the most sophisticated players will still make strong returns while supporting a cleaner, more flexible grid.

1. What MACSE and CM Really Mean for Green Technology

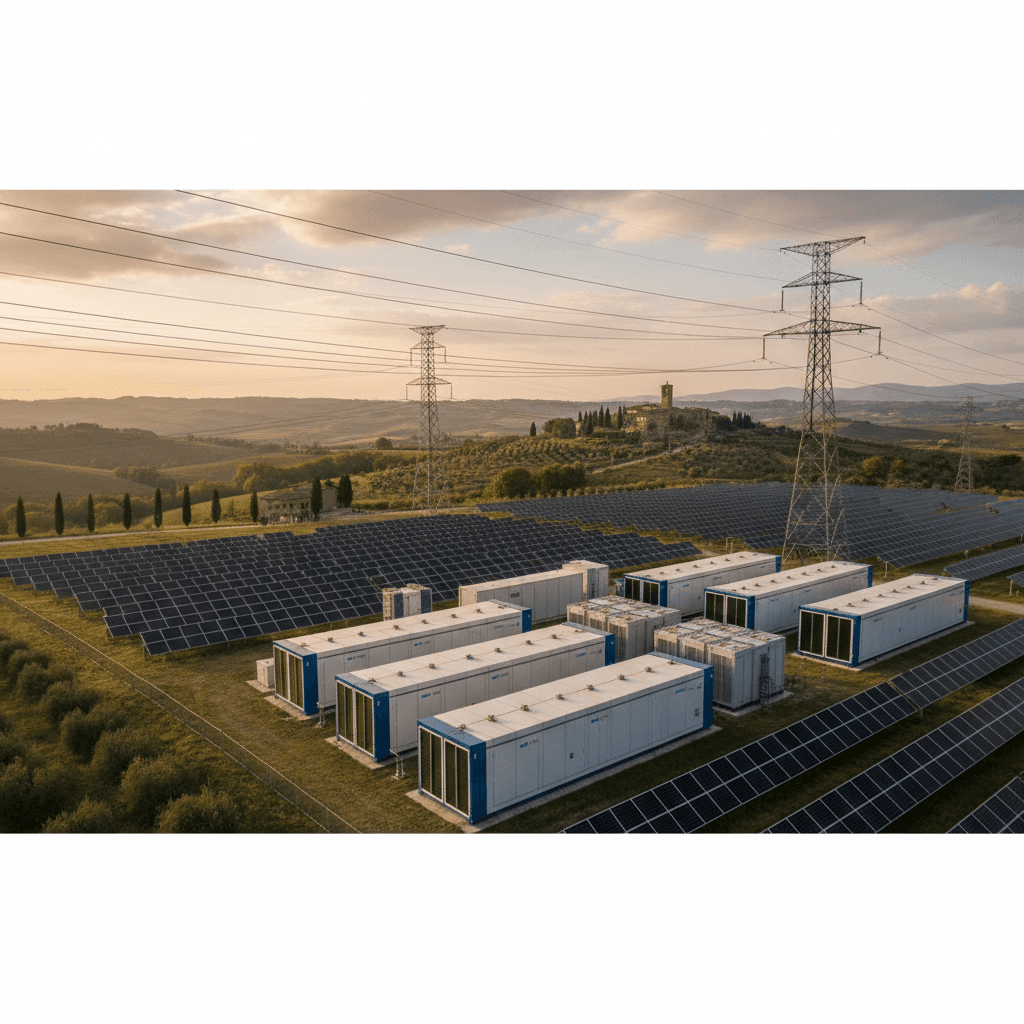

Italy’s MACSE auction and capacity market (CM) are long-term revenue anchors for grid-scale battery energy storage systems (BESS):

- MACSE: 15-year contracts for storage services to support system adequacy and flexibility.

- Capacity Market (CM): up to 15-year commitments for firm capacity available to the grid.

On paper, the first MACSE auction results looked brutal: very low tariffs, highly competitive bidding, and 10GWh awarded, with Enel taking roughly 65% of volumes. That sent a clear signal: big, integrated players with brownfield sites, scale in procurement and serious optimisation know-how now set the clearing price.

This matters for green technology because:

- Storage is now embedded in national reliability planning, not just a merchant side hustle.

- Long-term contracts make BESS bankable, which draws in institutional capital.

- The flip side is compressed headline revenues, so value has to be created via operations, not just contracts.

In other words, if the first wave of renewables was about building megawatts, this wave is about managing flexibility in megawatt-hours – intelligently.

2. How European BESS Asset Management Has Evolved

The European BESS market has shifted from “build and hope” to structured, risk-sharing models where optimisation is a core skill, not an afterthought.

Contracted vs merchant: two main playbooks

Most utility-scale storage portfolios today are run under one of two commercial models:

-

Contracted revenues (tolling-style)

- A trader or optimiser pays a fixed fee to the BESS owner.

- They take over commercial control and market participation for 5–7 years.

- The owner focuses on financing and technical performance; the trader takes price and optimisation risk.

-

Merchant with profit-sharing

- No guaranteed revenue; the asset is optimised across day-ahead, intraday, balancing and ancillary services.

- Revenues are split according to a predefined profit-sharing formula.

- Risk and upside are shared, which aligns incentives but demands confidence in both the trader and the optimisation stack.

In both cases, one constant remains: you need a strong route-to-market partner to handle:

- Physical dispatch into day-ahead and ancillary services markets

- Forecasting and bidding strategies

- Compliance with grid codes and TSO requirements

Financial tolling structures can simplify this (DA swaps, for instance), but they still depend on real-world dispatching management behind the scenes.

Why this shift matters now

As tariffs compress and competition grows, the old model of “secure a contract and relax” doesn’t work. Revenue stacking – smartly combining MACSE, CM, arbitrage and ancillary services – is where serious value is created.

And that’s exactly where AI and data-driven green technology show their worth.

3. The New Core Skill: AI-Driven Battery Optimisation

For MACSE and CM projects with low tariffs, precision optimisation is the difference between a mediocre IRR and a portfolio that quietly outperforms.

The operating decisions that matter

A high-performing BESS optimiser is constantly solving questions like:

- How do we split capacity between energy arbitrage, system services and contracted obligations each hour?

- How much cycling is justified given degradation costs and cell ageing models?

- What’s the optimal strategy given location-specific congestion and grid constraints?

- How should strategies change as renewables penetration and price volatility grow over the next 15 years?

Operators like Ego Energy describe themselves, accurately, as a one‑stop shop: they mix commercial trading expertise with plant-level technical knowledge, including:

- Plant modelling: accurate representation of BESS response, losses, limits and degradation.

- Real-time monitoring & control: IoT-based telemetry, SCADA integration and automated dispatch.

- Data-energy platforms: AI and data-science tools that learn from patterns in prices, demand and system behaviour.

The reality? MACSE tariffs might be low, but they’re fixed. Volatility in wholesale power and balancing markets, by contrast, is likely to increase as Italy adds more solar and wind. That means:

The relative value of flexible capacity rises over time, even if the nominal contract price looks thin on day one.

Smart operators will design strategies that harvest that rising optionality without burning through battery health.

4. Preserving Battery Health While Chasing Revenue

There’s a recurring mistake in early-stage storage markets: chasing every marginal euro and destroying cells in the process.

Sophisticated BESS asset managers do the opposite. They treat technical constraints as hard rules and build optimisation around them:

- Respect for operating windows (SoC, temperature, C-rates)

- Constraints on daily and lifetime cycles

- Firmware limits and OEM warranty conditions

From there, AI-enabled optimisation can:

- Quantify marginal degradation cost per cycle at different depths of discharge.

- Decide whether a given price spread is worth the wear.

- Adjust dispatch profiles during heatwaves or extreme events to protect cells.

I’ve found that the best operators think in long-term cashflow, not daily PnL. A trade that looks profitable today but shaves 0.2% off usable capacity permanently might not be worth it when your contract horizon is 15 years.

In the context of MACSE and CM, the formula is simple:

Guaranteed low tariffs + disciplined degradation management + smart revenue stacking = resilient long-term returns.

5. Risk-Sharing: Who Carries What in a Storage Project?

If you’re entering the Italian BESS market now, the real question isn’t “Are tariffs too low?” but “Who is actually holding the risk?”

Developer vs investor

For project development, the most common pattern is:

- The developer advances the project to key milestones: site control, permits, grid connection, revenue contracts (MACSE/CM, PPAs for co-located assets).

- The investor pays staged earn-outs as each milestone is achieved, up to final contract validation.

This structure:

- Rewards developers for de-risking, not just originating.

- Protects investors against early-stage project failure.

- Shortens payback for developers, enabling them to recycle capital.

Asset owner vs trader/optimiser

Then comes the operational layer:

- Tolling agreement: the trader/optimiser takes almost all commercial risk in exchange for a fixed payment. This suits conservative investors who want visibility and stable cashflows.

- Profit-sharing: both parties share risk and upside, which suits more return-seeking capital and highly confident traders.

In both cases, if you’re the asset owner, you should be laser-focused on three questions:

- How strong is the optimiser’s track record and technology stack?

- How clearly are technical constraints and performance guarantees defined in the contract?

- Does the risk-sharing model match your fund mandate and time horizon?

Most companies get this wrong by optimising only for headline price or fee. The smarter move is to optimise for aligned incentives and long-term resilience – especially in a system like Italy’s, where competition will keep growing.

6. Standalone vs Co-Located BESS: What Changes in Italy?

In many markets, co-locating storage with renewables fundamentally changes the economics. In Italy, the picture is more nuanced.

Under rules from the Italian energy authority (ARERA):

- There’s basically no difference in energy cost to charge the BESS whether it’s physically connected to a co-located plant or not.

So what’s the point of co-location?

The commercial edge of flexible PPAs

Traders and offtakers still like co-located setups because:

- Storage introduces flexibility into PPA pricing. You’re no longer locked into strict baseload or “as-produced” profiles.

- You can shape delivery to the market or to an offtaker’s needs, which tends to improve PPA terms.

And this doesn’t even have to be physical. Virtual co-location (commercially linking a standalone BESS to a remote solar/wind plant under a shared optimisation and PPA structure) can achieve similar benefits.

From a green technology perspective, co-location and virtual hybrids are important because they:

- Help integrate more renewables without curtailment.

- Reduce grid stress by smoothing output.

- Give developers more ways to structure bankable, flexible clean energy contracts.

7. Why MACSE Revenues Should Become More Competitive Over Time

On day one, low MACSE tariffs look like a squeeze. Over a 15-year horizon, they’re more like cheap entry tickets to a volatility-rich, renewables-heavy grid.

Here’s why those contracted revenues should become relatively more attractive:

-

Rising renewables share

Italy is on track to add large volumes of solar and wind. More non-dispatchable generation means more imbalance, more intraday volatility and more need for flexible capacity. -

Structural volatility, not just seasonal spikes

As penetration grows, price cannibalisation at midday and scarcity in peak hours become structural, not occasional. Batteries that can move energy across hours and provide reserves will become system-critical assets. -

Regulatory focus on system reliability

TSOs and regulators don’t like blackouts. As dependency on renewables increases, they will continue to support mechanisms – like MACSE and CM – that reward firm flexible capacity. -

Technological edge compounds

The operators who learn fastest now will have the data, models and processes to extract more value from every kWh of stored energy later. Their cost of optimisation per MW will keep falling.

In practice, this means:

The value of a MACSE-backed battery is likely to improve relative to the rest of the market as the system gets “noisier” and more renewable-heavy.

The blunt truth is that early, aggressive bidders like Enel are betting not just on cheap hardware and brownfield sites, but on their ability to run these assets brilliantly.

Where This Fits in the Green Technology Story – And What You Can Do Next

Battery optimisation in Italy’s MACSE and capacity markets isn’t just an investment story; it’s a core piece of the green technology transition. Flexible storage:

- Makes higher shares of renewables actually workable.

- Reduces curtailment and wasted clean energy.

- Cuts reliance on fossil peakers and supports grid stability.

If you’re:

- An investor: focus less on headline tariff levels and more on who is operating the assets, how they manage degradation, and how they stack revenues.

- A developer: build projects to a standard that serious optimisers want to manage – robust data, clear constraints, flexible commercial structures.

- A technology or AI player: there’s huge room to add value with forecasting, optimisation engines, degradation modelling and route-to-market automation.

The next phase of green technology growth won’t be won by whoever installs the most batteries; it’ll be won by whoever operates them smartest in markets like Italy’s.