Germany’s latest 213MWh of battery storage shows how green technology, smart finance and AI-driven optimisation are reshaping profitable clean energy.

Most companies still talk about “going green” as if it’s a CSR line item. Meanwhile, Germany is quietly wiring hundreds of megawatt-hours of battery storage directly into its power markets – and making serious money while cutting emissions.

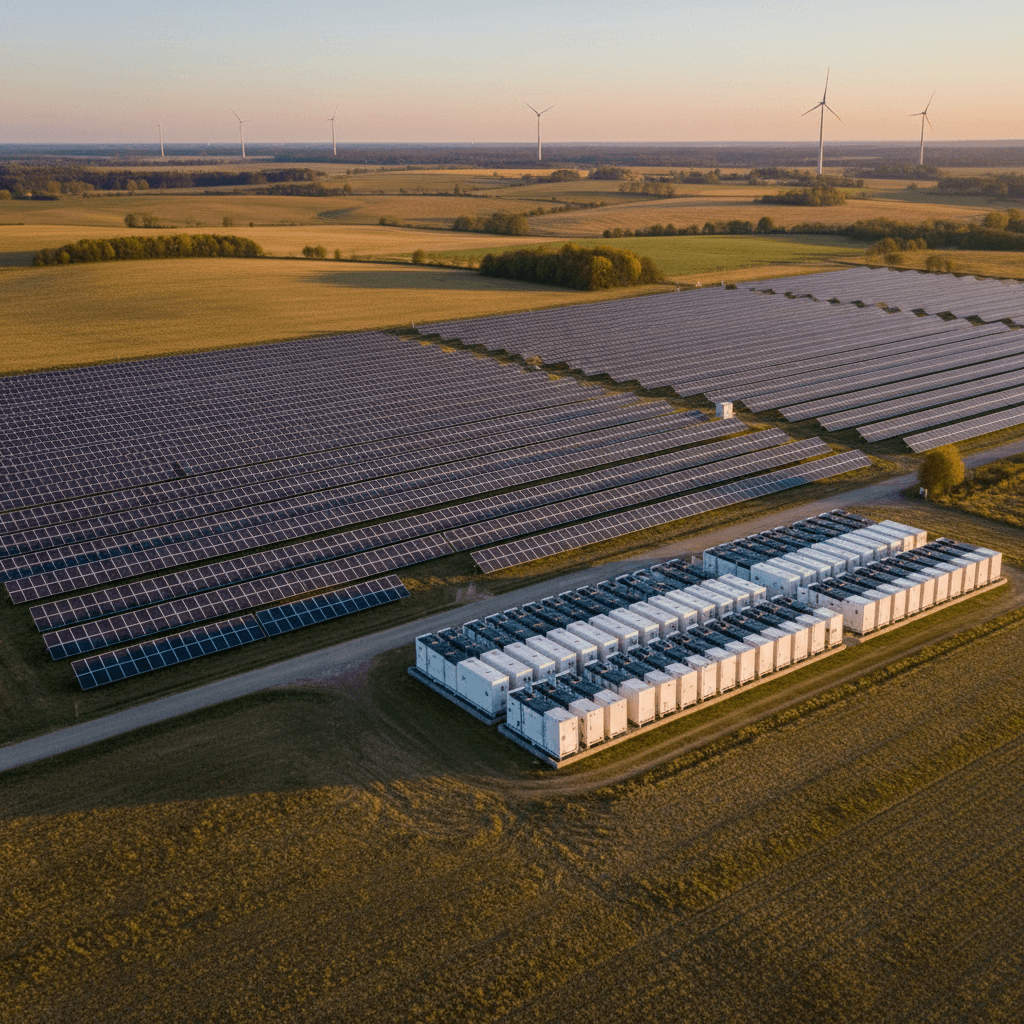

The latest example: Statkraft, Kyon Energy and Juniz Energy have collectively advanced 213MWh of battery energy storage systems (BESS) in Germany. On the surface it’s just another set of project announcements. Look closer and you see a blueprint for how green technology, smart finance and AI-driven energy optimisation fit together.

This matters because the energy transition is no longer about installing more solar and wind. It’s about making clean energy dispatchable and profitable – and that’s where BESS, intelligent software and new business models come in.

In this post, I’ll break down what’s actually happening in Germany, why investors and operators care, and how these storage projects illustrate the next phase of green technology – especially for anyone building or funding clean energy assets.

Germany’s 213MWh BESS wave at a glance

Germany’s storage market is shifting from pilot projects to industrial scale. The three headline moves are:

- Statkraft has commissioned a hybrid solar-plus-storage plant with a 16MW/57MWh BESS.

- Kyon Energy, backed by TotalEnergies, is building a 20.7MW/56MWh BESS with Canadian Solar’s e-Storage technology.

- Juniz Energy has secured financing for around 100MWh of standalone BESS across three projects.

All three sit inside a much bigger trend. In just the last weeks, Germany has seen projects around 700MWh each move into construction and a 1GW/4GWh project announced for 2027/28. Storage isn’t a side show anymore; it’s becoming core infrastructure.

The reality? Germany has become Europe’s most attractive BESS market because:

- Wholesale prices are volatile, creating huge arbitrage spreads.

- Regulations have been updated to treat storage more fairly (for example, reducing double-charging of grid fees).

- Banks and infrastructure funds now understand the revenue stack and are willing to finance multi-project pipelines.

If you’re working anywhere near green technology, this combination of hardware, software and finance is exactly what the next 10 years will look like.

Inside Statkraft’s hybrid solar-plus-storage project

The Statkraft project shows how hybrid renewable plants are becoming the new normal.

- Capex: About €45 million

- Solar: 46.4MW

- Battery: 16MW/57MWh, made up of 88 battery cubes

- Location: Zerbst, Germany

- Support scheme: Germany’s EEG “innovation tender” for hybrid plants

Why this project matters

Germany’s innovation tender doesn’t just subsidise solar; it specifically rewards hybrid projects where storage is tightly integrated. The storage system must be charged from the renewable plant, not just the grid. That pushes developers to build systems that:

- Smooth the solar output profile

- Avoid curtailment during midday oversupply

- Shift energy into peak pricing hours

- Support local grid stability

From a green technology perspective, this is smart policy. It doesn’t just subsidise clean generation; it subsidises clean flexibility.

Where AI and software come in

A hybrid plant like this only earns its full potential if it’s optimised in real time. That’s largely a software and AI problem, not a hardware one.

In practice, that means:

- Forecasting solar generation minute-by-minute

- Predicting intraday and day-ahead prices

- Managing state of charge so the battery is “in the right place at the right time”

- Arbitraging across multiple value streams (wholesale, balancing, possibly ancillary services)

I’ve seen operators underestimate this repeatedly. They treat the battery like a static asset when it’s essentially an algorithmic trading machine physically tied to a transformer. The winners are going to be the ones who invest as much in optimisation software – and talent – as they do in the containers themselves.

Kyon Energy, Canadian Solar and the quiet shift in BESS supply

The second move is a 20.7MW/56MWh BESS project in Lower Saxony, developed by Kyon Energy and supplied by Canadian Solar’s e-Storage arm (using its Solbank platform). Commissioning is targeted for late 2026, with shipments starting in March.

On paper it’s a straightforward grid-scale BESS project. The more interesting story sits behind it.

Why using a “non-group” BESS supplier is a big signal

Kyon is owned by TotalEnergies, which also owns the BESS integrator Saft. Saft is already providing systems for 321MW of Kyon-developed projects in Germany.

So why is Kyon using Canadian Solar’s BESS on this one?

Because the storage market is now competitive enough that even vertically integrated energy majors are:

- Shopping around on technology (cycle life, thermal design, DC efficiency, footprint)

- Diversifying suppliers to reduce risk in their build-out programs

- Optimising total cost of ownership, including 20-year long-term service agreements

This is a sign of a maturing industry: hardware is modular, supply chains are flexible, and the real differentiation is often in software, O&M and financing.

How this fits the green technology narrative

Kyon’s project is a textbook example of how green technology is no longer just “clean energy hardware”. It’s a layered stack:

- Physical assets – BESS containers, inverters, transformers

- Digital layer – SCADA, battery management systems, AI-based dispatch optimisation

- Financial layer – LTSAs, project finance, hedging, and potential future asset sales

The value is created at the intersection of the three. If you remove the digital and financial layers, the IRR collapses. If you remove the physical layer, there’s nothing to optimise in the first place.

For investors and developers, the lesson is simple: don’t treat BESS decisions as pure capex procurement. The technology choice locks in your software options, your O&M regime and the bankability of your cash flows for two decades.

Juniz Energy: why 100MWh of financed storage is a bigger deal than it looks

The Juniz Energy story is less photogenic – no big commissioning photos, just a financing announcement. But strategically, it might be the most important of the three.

Juniz, owned by private equity firm EQT, has secured financing from Hamburg Commercial Bank (HCOB) for three BESS projects totaling around 100MWh. HCOB is acting as:

- Lender

- Agent

- Account bank

- Hedging bank

That’s a full-stack banking relationship wrapped around flexible, grid-scale green infrastructure.

Why this kind of financing structure matters

When one bank is comfortable taking multiple roles across a 100MWh portfolio, it tells you a few things:

- The revenue model is now well understood (arbitrage, balancing markets, possibly local services)

- The technology risk is considered manageable over the life of the loan

- The policy risk in Germany has decreased enough to make storage bankable

This is exactly what unlocks scale. Once a bank writes term sheets for three assets, writing term sheets for thirty isn’t a huge leap.

For green technology more broadly, this is the inflection point. Clean hardware stopped being exotic the moment banks started treating it like a repeatable product, not a science experiment.

What this means for developers, investors and large energy users

These 213MWh in Germany aren’t just news items; they’re a set of very practical signals for anyone working in energy or sustainability.

1. Storage is now central to project design, not an add-on

If you’re still designing utility-scale solar or wind without at least stress-testing a co-located BESS, you’re behind. The Statkraft project under the innovation tender is a clear nudge in one direction: hybrids are the standard model going forward.

Developers should be asking:

- How much curtailment can storage avoid at my site?

- What’s the optimal battery duration for my revenue mix (2, 4, or more hours)?

- How does co-location affect grid fees, land use and permitting timelines?

2. AI-driven optimisation is not optional anymore

Every MWh in these systems will be dispatched by algorithms, not spreadsheets. To compete in markets with:

- Intraday volatility

- Real-time balancing products

- Complex grid constraints

…you need software that can make thousands of micro-decisions per day about charging, discharging and state-of-health management.

If you’re a large energy user or corporate buyer, this is an opportunity too. Partnering with storage operators who use advanced optimisation tools can:

- Reduce your exposure to price spikes

- Improve the carbon profile of your energy consumption

- Turn your sites into flexible assets supporting the grid

3. Financing is evolving, and so should your strategy

Juniz’s deal with HCOB shows that banks will fund storage when the structure is right. Practically, that means:

- Strong route-to-market agreements (e.g., with trading houses or optimisers)

- Bankable technology with a clear track record

- Thoughtful risk allocation in LTSAs and EPC contracts

If you’re building a pipeline, you’ll get better terms when:

- The projects share common contracts and technology

- The revenue stack is diversified across services

- You can evidence robust optimisation (again, software and AI)

The days of “we’ll just plug a battery in and figure out revenues later” are over.

How this fits into the broader green technology shift

Zoom out from Germany and the pattern is consistent with everything we’ve been covering in this Green Technology series:

- Clean energy is becoming data-rich and software-defined.

- AI isn’t a buzzword add-on; it’s how storage assets and grids stay profitable and stable.

- The line between infrastructure and technology is blurring.

Solar panels made renewable energy cheap. Battery energy storage systems – intelligently operated – are making it reliable, flexible and investable at scale.

If you’re a developer, investor or corporate energy buyer, the next step is simple:

- Treat batteries as core strategic assets, not compliance tools.

- Build or partner for serious optimisation capabilities.

- Look for markets, like Germany, where policy and pricing already reward flexibility.

The projects from Statkraft, Kyon and Juniz won’t be the largest we see in Europe – not for long. But they’re a clear signal of where green technology is heading: a grid where clean power, smart storage and AI-driven control systems work together as one integrated system.

The question now is less “will this scale?” and more “how quickly can you align your own strategy with this new reality?”