Name matching is reducing payment errors and fraud by verifying beneficiary names before funds move. Here’s how banks and fintechs can implement it fast.

Name Matching in Payments: Fewer Errors, Less Fraud

Payment errors are rarely “just ops issues.” They’re risk issues, cost issues, and customer-experience issues—especially when money moves fast and disputes move slow.

That’s why the small-sounding improvement in the RSS headline—Prometeo improving payment accuracy across the US with name matching—deserves more attention than it’s getting. Name matching is one of those behind-the-scenes checks that can turn messy, expensive payment workflows into something far more predictable. And the interesting part for Australian banks and fintechs: the same approach maps cleanly onto local challenges like AML/CTF compliance, fraud prevention, and cross-border payment accuracy.

This post breaks down what name matching actually does, why it’s suddenly showing up in payment stacks, how it connects to AI in finance, and what a practical rollout looks like if you’re running payments, risk, or product.

Name matching is a simple idea with outsized impact

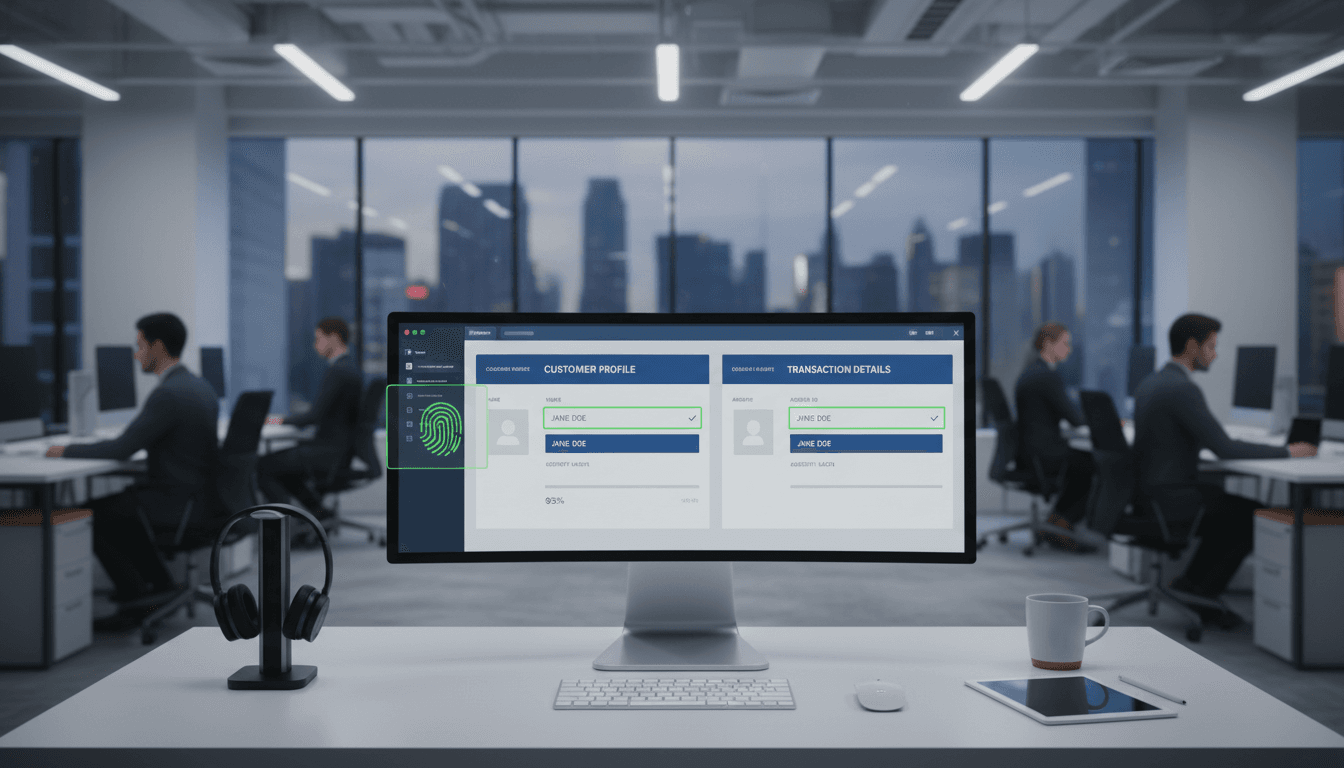

Name matching improves payment accuracy by verifying that the payer-entered beneficiary name aligns with the account holder’s name before the payment is sent. If there’s a mismatch, the payment can be flagged, paused, or routed for review.

That sounds basic, but it targets a stubborn problem: human-entered identity data is messy. People abbreviate, swap first/last names, change surnames, include middle initials, use business trading names, or paste in extra punctuation. Meanwhile, criminals exploit those same inconsistencies to redirect funds.

Where payment errors really come from

In real payment flows, “wrong recipient” incidents tend to come from a few patterns:

- Mistyped beneficiary details (name doesn’t match account, but the transfer still goes out)

- Invoice fraud and business email compromise (BEC) (the details are “valid,” but belong to a fraudster)

- Lookalike beneficiaries (similar names inside payroll/AP lists)

- Legacy customer data (CRM name differs from bank account name)

Name matching doesn’t solve everything on its own, but it’s one of the most cost-effective controls because it catches both accidental and malicious misdirection.

“Name matching” isn’t one thing

There are different levels of sophistication:

- Exact matching: fast, brittle, high false positives

- Fuzzy matching: tolerates spelling variations and formatting

- Entity-aware matching: understands individuals vs businesses, common abbreviations, suffixes, trading names

- Risk-based matching: uses context (amount, payee novelty, device, geo, velocity) to decide how strict to be

Once you get into fuzzy/entity-aware/risk-based matching, you’re effectively in AI-assisted payments verification territory.

Why name matching shows up now (and why the US matters)

The US has historically had fewer standardized pre-payment verification controls than some other markets, so accuracy upgrades deliver immediate ROI. When a provider announces better payment accuracy across a huge market, it usually means two things are happening:

- Payment rails and bank integrations are modernizing quickly.

- Fraud pressure is forcing better “verify-before-you-send” controls.

Even without the full press article text (the source page was blocked behind a verification step), the direction is clear: fintech infrastructure providers are productizing name matching as a standard capability—because banks, billers, and platforms are tired of cleaning up preventable mistakes.

Australia already cares about this—just under different labels

In Australia, the problem statement is familiar:

- Faster payments mean faster fraud and less time to recover funds.

- Regulators and boards expect stronger controls, not just “we refunded the customer.”

- Cross-border and multi-rail experiences require consistent verification.

Many teams talk about this as payee verification, beneficiary validation, or confirmation-style checks. Whatever you call it, the business goal is the same: reduce misdirected payments and reduce fraud losses without destroying conversion.

How AI-powered name matching works in practice

The best name matching systems combine deterministic rules with machine learning to reduce false positives while still blocking real risk.

If you’ve ever shipped “simple” matching logic, you’ve seen the trade-off:

- Too strict → customers fail checks and churn

- Too loose → fraud slips through and disputes spike

AI helps by learning which mismatches are harmless (formatting, nicknames, word order) and which are meaningful (entirely different surname, unrelated business entity, suspicious token patterns).

A practical matching pipeline (what’s typically happening)

A production-grade pipeline often includes:

-

Normalization

- Lowercasing, removing punctuation, stripping extra whitespace

- Transliteration where needed (cross-border use cases)

-

Tokenization and weighting

- Separating first/last names, business suffixes (

pty,ltd,inc) - Down-weighting noisy tokens (like “trading as” patterns)

- Separating first/last names, business suffixes (

-

Similarity scoring

- String distance measures (e.g., edit distance) plus phonetic similarity

- Embedding-based similarity for more complex cases

-

Entity logic

- Individual vs business matching rules

- Handling joint accounts or multi-party beneficiaries

-

Decisioning

- Pass / Warn / Block

- Routing to step-up verification for higher-risk transactions

A line I’ve found useful when socialising this internally: “We’re not trying to prove identity with a name. We’re trying to spot when the name strongly suggests the money is headed to the wrong place.”

Reducing fraud without adding friction

Done well, name matching supports a risk-based customer experience:

- Low-risk mismatch → soft warning (“Name doesn’t look right. Double-check.”)

- Medium-risk mismatch → require confirmation or second factor

- High-risk mismatch → block and prompt review

That keeps conversion healthy while still meaningfully reducing fraud.

Where name matching fits in a modern fintech stack

Name matching is most valuable when it’s treated as a reusable service, not a one-off feature inside a single product. If you’re a bank, PSP, lender with disbursements, or fintech platform managing payouts, it can sit in a few places:

- At payee creation (best moment to prevent future mistakes)

- Pre-payment validation (especially for first-time payees)

- Batch payments (payroll, AP runs, gig worker payouts)

- Cross-border payments (extra value when data formats vary)

The compliance angle: AML/CTF and sanctions screening

Name matching also plays well with compliance, but teams need to keep the concepts distinct:

- Payee name matching: “Is this the intended recipient?”

- Sanctions/PEP screening: “Is this person/entity prohibited or high risk?”

The technology overlaps (entity resolution, fuzzy matching), but the objectives, thresholds, and governance differ. Mixing them carelessly creates confusing customer outcomes and messy audit trails.

The data quality angle: your biggest hidden blocker

Most orgs discover this quickly: your internal customer/payee names are inconsistent across systems.

If you want name matching to work, invest early in:

- A single canonical representation of the beneficiary name

- Clear rules for business names vs trading names

- Feedback loops from exceptions (why did it mismatch?)

Name matching is a control, but it’s also a mirror. It shows you where your data hygiene is weak.

Implementation playbook for banks and fintechs (Australia-focused)

A successful rollout starts with measuring today’s “badness,” then introducing name matching with controlled friction. Here’s a practical approach I’d use.

1) Pick a narrow, high-impact use case

Start where error rates or fraud exposure are highest:

- First-time payees

- High-value transfers

- Accounts payable vendor onboarding

- Marketplace payouts where beneficiary details change frequently

Narrow scope reduces political friction and makes ROI easier to prove.

2) Define outcomes using numbers (not vibes)

Good baseline metrics include:

- Payment exception rate (returns, recalls, disputes)

- Misdirected payment incidents per 10,000 transfers

- Fraud losses tied to beneficiary changes

- Customer support contacts per 1,000 payments

- Conversion impact (drop-off at payee setup / send)

If you can’t quantify improvement, the feature becomes “nice to have” during the next budget squeeze.

3) Use a three-tier decision model: Pass / Warn / Block

Most companies get this wrong by going straight to “block.” A better way:

- Pass: high confidence match

- Warn: medium confidence mismatch, allow user confirmation

- Block: low confidence, high risk, or policy violation

This is where AI-assisted scoring shines: it’s not binary.

4) Build an exception workflow that doesn’t drown ops

Name matching creates exceptions. Plan for them.

- Provide agents with why it mismatched (token-level explanation)

- Log the input, the reference name, and the score for audit

- Add a learning loop: confirmed good matches should reduce future friction

5) Treat it as part of your fraud stack, not a standalone feature

Name matching is strongest when paired with:

- Device and session risk signals

- Beneficiary change monitoring

- Velocity controls (new payee + high amount + urgent timing)

- Behavioural analytics

Fraudsters adapt. Single controls age quickly.

People also ask: quick answers

Does name matching prevent invoice fraud?

It helps, but it’s not a silver bullet. If a fraudster convinces a business to pay a new account name that looks plausible, name matching can still catch mismatches—especially when the legitimate vendor name is known and consistent. It’s most effective when paired with vendor onboarding controls and beneficiary change verification.

Won’t name matching create false positives for multicultural names?

It can, unless the system is designed for real-world diversity. Good implementations handle different name orders, compound surnames, transliteration, and common abbreviations. This is one reason ML-assisted matching tends to outperform strict rules.

Where should we apply name matching first?

At payee creation and first payment. Those two steps catch most preventable errors while limiting friction for repeat payments.

What this signals for AI in Finance and FinTech in 2026

Name matching is a perfect example of what I like about practical AI in finance: it’s not flashy, but it pays for itself. It reduces wasted ops time, prevents avoidable losses, and makes compliance and fraud teams less reactive.

For Australian banks and fintechs, the bigger story is structural: AI is increasingly being embedded into everyday financial transactions as “micro-controls.” Customers don’t see “AI.” They see fewer mistakes, fewer scams, and fewer painful support calls.

If you’re evaluating name matching (or already using it and not seeing results), the next step is to run a tight pilot: pick one flow, set measurable targets, and instrument the hell out of exceptions. The question worth asking internally isn’t “Should we use AI here?” It’s “Where are we still letting preventable payment errors through, and what would it cost to stop them?”